夜雨聆风

夜雨聆风

一个万能指标公式,代码简洁且功能强大

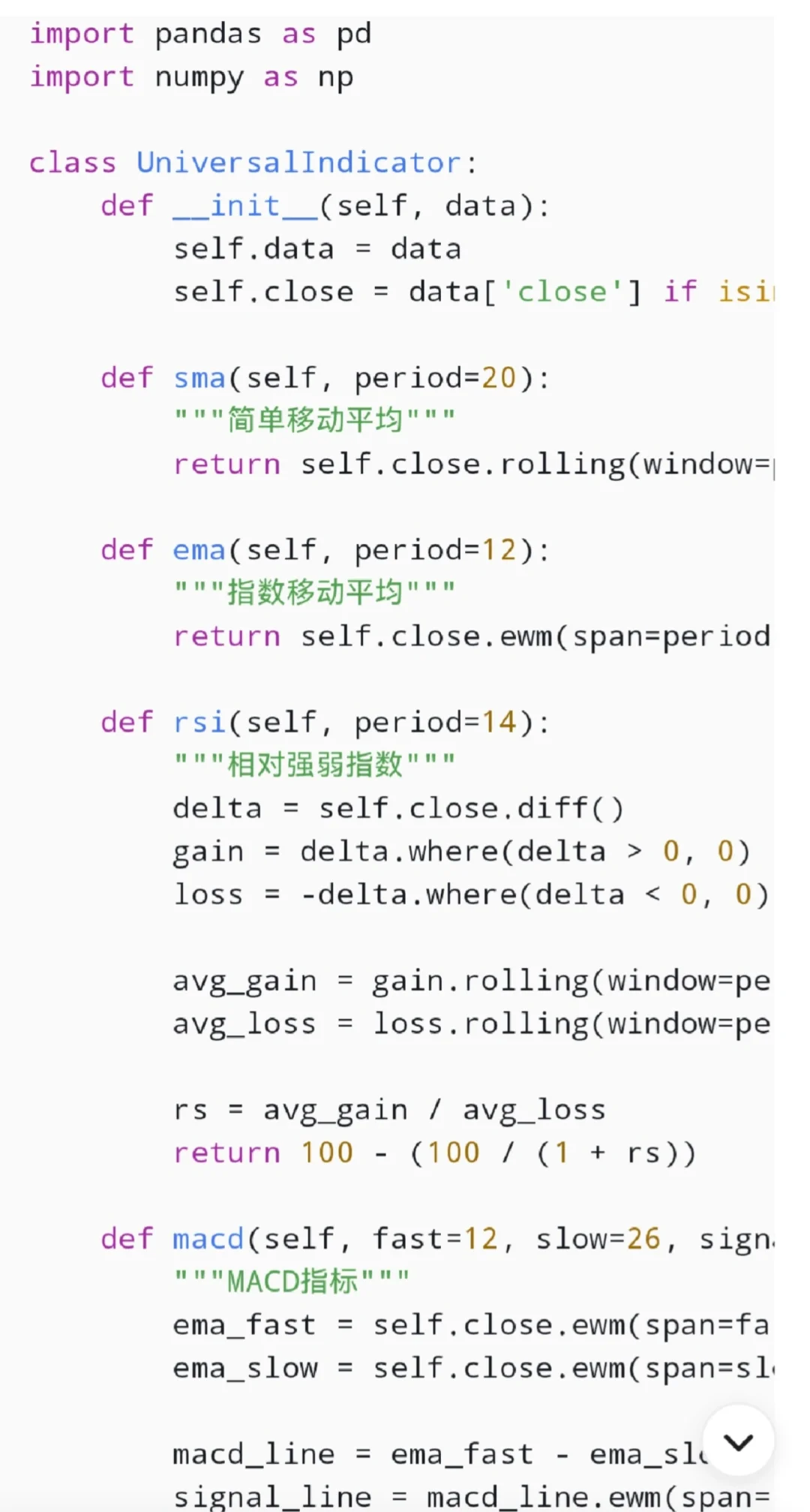

import pandas as pd

import numpy as np

class UniversalIndicator:

def __init__(self, data):

self.data = data

self.close = data[\’close\’] if isinstance(data, pd.DataFrame) else data

def sma(self, period=20):

\”\”\”简单移动平均\”\”\”

return self.close.rolling(window=period).mean()

def ema(self, period=12):

\”\”\”指数移动平均\”\”\”

return self.close.ewm(span=period, adjust=False).mean()

def rsi(self, period=14):

\”\”\”相对强弱指数\”\”\”

delta = self.close.diff()

gain = delta.where(delta > 0, 0)

loss = -delta.where(delta < 0, 0)

avg_gain = gain.rolling(window=period).mean()

avg_loss = loss.rolling(window=period).mean()

rs = avg_gain / avg_loss

return 100 – (100 / (1 + rs))

def macd(self, fast=12, slow=26, signal=9):

\”\”\”MACD指标\”\”\”

ema_fast = self.close.ewm(span=fast).mean()

ema_slow = self.close.ewm(span=slow).mean()

macd_line = ema_fast – ema_slow

signal_line = macd_line.ewm(span=signal).mean()

histogram = macd_line – signal_line

return macd_line, signal_line, histogram

def bollinger_bands(self, period=20, std=2):

\”\”\”布林带\”\”\”

sma = self.sma(period)

rolling_std = self.close.rolling(window=period).std()

upper = sma + (rolling_std * std)

lower = sma – (rolling_std * std)

return upper, sma, lower

def stochastic(self, k_period=14, d_period=3):

\”\”\”随机指标\”\”\”

low_min = self.data[\’low\’].rolling(window=k_period).min()

high_max = self.data[\’high\’].rolling(window=k_period).max()

k_line = 100 * ((self.close – low_min) / (high_max – low_min))

d_line = k_line.rolling(window=d_period).mean()

return k_line, d_line

def atr(self, period=14):

\”\”\”平均真实波幅\”\”\”

high = self.data[\’high\’]#oc #算法 #量化

import numpy as np

class UniversalIndicator:

def __init__(self, data):

self.data = data

self.close = data[\’close\’] if isinstance(data, pd.DataFrame) else data

def sma(self, period=20):

\”\”\”简单移动平均\”\”\”

return self.close.rolling(window=period).mean()

def ema(self, period=12):

\”\”\”指数移动平均\”\”\”

return self.close.ewm(span=period, adjust=False).mean()

def rsi(self, period=14):

\”\”\”相对强弱指数\”\”\”

delta = self.close.diff()

gain = delta.where(delta > 0, 0)

loss = -delta.where(delta < 0, 0)

avg_gain = gain.rolling(window=period).mean()

avg_loss = loss.rolling(window=period).mean()

rs = avg_gain / avg_loss

return 100 – (100 / (1 + rs))

def macd(self, fast=12, slow=26, signal=9):

\”\”\”MACD指标\”\”\”

ema_fast = self.close.ewm(span=fast).mean()

ema_slow = self.close.ewm(span=slow).mean()

macd_line = ema_fast – ema_slow

signal_line = macd_line.ewm(span=signal).mean()

histogram = macd_line – signal_line

return macd_line, signal_line, histogram

def bollinger_bands(self, period=20, std=2):

\”\”\”布林带\”\”\”

sma = self.sma(period)

rolling_std = self.close.rolling(window=period).std()

upper = sma + (rolling_std * std)

lower = sma – (rolling_std * std)

return upper, sma, lower

def stochastic(self, k_period=14, d_period=3):

\”\”\”随机指标\”\”\”

low_min = self.data[\’low\’].rolling(window=k_period).min()

high_max = self.data[\’high\’].rolling(window=k_period).max()

k_line = 100 * ((self.close – low_min) / (high_max – low_min))

d_line = k_line.rolling(window=d_period).mean()

return k_line, d_line

def atr(self, period=14):

\”\”\”平均真实波幅\”\”\”

high = self.data[\’high\’]#oc #算法 #量化