夜雨聆风

夜雨聆风

5月12日 新湖-时瑞中国国际化商品综合指数(XSCI)收于219.28(+0.53,+0.244%)。

*欲了解指数的更多详情,请点击左下方阅读原文。

Mr. Hou Zhenhai

Straits Group Chief Strategist

Review of Last Views:

Main Points:

1. AI investment has become the sole decisive factor driving the current global market. By contrast, the impact of international geopolitical developments, oil prices, macroeconomic data and even Fed policies on the market have weakened markedly.

2. The reasons: 1, AI investment has become the only certain growth driver in the market. 2, the rapid growth of AI investment is decoupled from macroeconomic trends and also independent of the monetary policies of global central banks. 3, AI investment today features a highly capital-intensive nature, meaning most of AI investment gains are within the corporate /shareholder sector or are converted into fixed assets, with only a minimal share going toward labor income. 4, hence the semiconductor and related hardware industries will see a substantial surge in profits. Since March, earnings forecasts upward revision for US stocks have hit a record high, most coming from AI-related stocks, particularly semiconductor hardware.

3. The AI-driven K-shaped divergence will deepen, with the divergence in earnings and market capitalization also widening across stock sectors and individual stocks. But stagnant household income will keep consumer stocks underperforming tech hardware stocks. Meanwhile, capex pressure drives most cash demand on US tech companies, esp. the leading cloud service giants, which have to tap the global corp debt market more often to maintain their capex.

4. China’s economy pattern remains “output stronger than consumption and exports stronger than domestic demand”. Households begin to deleverage, which may still weight on consumption sector performances.

5. Even if oil prices ease slightly in the short term, previous supply disruptions and inventory drawdowns will keep oil prices elevated for an extended period ahead, thereby continuing to weigh on global consumption. Stocks closely linked to global retail consumption will continue to suffer from weak demand and elevated energy costs. Global investable capital will keep converging toward AI hardware-related stocks with clear growth prospects, further intensifying the market’s K-shaped divergence.

6. US, A-share and Hong Kong stock markets may maintain K-shaped divergence in the near term. For instance, the Nasdaq will outperform the Dow Jones, while the ChiNext Index will outperform the Shanghai Composite Index. Nevertheless, after the sharp rally over the past month, major market indices are expected to see a slower pace of gains following the pricing-in of positive sentiment from the US-Iran ceasefire.

7. With market focus rotating back toward AI investment, base metals will have better upside potential than the previously strong energy and chemical sectors. Gold and silver are also set to stage a moderate rebound.

Since the outbreak of the US-Iran war in March, geopolitical tensions have deteriorated. Disruptions to supplies through the Strait of Hormuz have triggered a sharp surge in oil prices, posing major risks to the global economy this year. Nevertheless, after a pullback in March, global stock markets staged a sustained rebound starting in April, with major stock indices in the US, South Korea and some others hitting record highs. A fundamental shift has taken place in stock market dynamics before and after the outbreak of the war. Prior to the conflict, global stock market hotspots were relatively diversified, whereas the current round of global equity rebounds has become highly concentrated on AI capex-related themes. It is evident that the performance of stock markets and individual stocks since April has been entirely determined by their connection with AI capex, and especially the related hardware demand. For instance, the Philadelphia Semiconductor Index in the US skyrocketed from 7,084 points to 12000 points in just 30 trading days from early April to the present, representing a gain of over 60%. Taiwan and South Korea’s stock markets have led global gains since the start of this year, solely due to the heavy weighting of semiconductor stocks in their respective markets. Similarly, semiconductor and optical module stocks have led the rally in the A-share market. Since global stock markets resumed their upward momentum in April, semiconductor and other hardware manufacturers benefiting from AI capex have become the sole decisive factor driving the current global market. By contrast, the impact of international geopolitical developments, oil prices, macroeconomic data and even Fed policies on the market have weakened markedly.

We believe the above phenomenon can be attributed to the following reasons. First, against the backdrop of highly uncertain global geopolitics and economic trends, AI investment has instead become the only certain growth driver in the market. Consequently, the more volatile and unstable global political and economic conditions become, the more capital is forced to pivot toward AI-related investment opportunities. In other words, the certainty of AI growth stands as its greatest scarcity premium amid an uncertain global economic environment. As a result, capital from all countries and other sectors worldwide has increasingly flowed into AI-related industries, either through secondary market stock purchases or PE/VC investments. This has created a powerful capital siphon effect for AI investments, triggering an explosive surge in valuations across relevant industries and individual stocks.

Second, at the current stage, the rapid growth of AI investment is decoupled from macroeconomic trends and also independent of the monetary policies of global central banks. This is because AI has evolved into a core development direction that major global tech giants are competing fiercely for and collectively betting on, ensuring that AI investment will maintain robust growth for the foreseeable future. This also means AI investment is essentially disconnected from current global macroeconomic performance. Merely the estimated total AI investment by US tech giants this year—akin to an arms race—will exceed US$800billion. Such massive spending leaves these companies with no room to back down until the final competitive outcome is decided. Hence their AI capital expenditure is completely insulated from fluctuations in the macroeconomy or international geopolitical situations. Meanwhile, these tech giants boast abundant capital strength and strong financing capacity, enabling them to sustain and ramp up heavy capital spending on AI over the next year, regardless of Fed rate moves, hikes or cuts. From this perspective, uncertain events such as the US-Iran conflict and the leadership change at the Fed may weigh on other global sectors, especially cyclical consumption. Therefore they further highlight the scarcity of AI’s guaranteed growth this year, boosting its appeal to global capital.

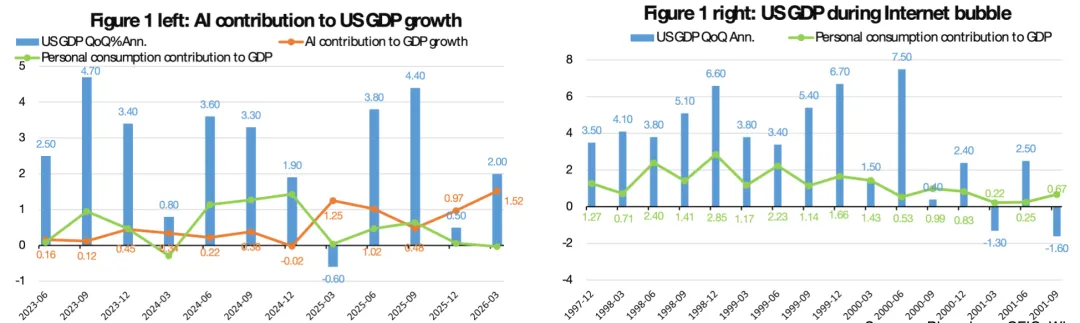

Third, AI investment today features a highly capital-intensive nature. Compared with the Internet bubble three decades ago, the capitalization ratio of the current AI investment wave is markedly higher. While both booms drove hardware investment, the Internet era mainly fueled demand for network telecom equipment and computer hardware, with an overall scale far smaller than the current AI-driven demand for computing power, high-speed storage, data centers and even power infrastructure construction. In addition, the rise of the Internet bubble generated massive demand for software and talent, meaning a far larger share of investment flowed to labor compensation than is the case today. By contrast, AI investment today creates far fewer new job opportunities, while instead replacing more service-sector jobs. Even overall employment in Silicon Valley in the US is now declining. Overall, nearly the bulk of AI investment flows to the capital side, including technological R&D and hardware deployment, with only a very limited portion allocated to the labor income. The upside of this model is that for the same scale of investment, a higher capitalization ratio better supports profit expansion and stock price gains for AI-related manufacturers along the industrial chain. The downside is that aggregate labor income does not rise, which may further suppress overall consumption. As shown in the left chart of Figure 1: over the past six months, US economic growth has slowed noticeably overall, yet the growth rate of AI investment and its contribution to US GDP have kept rising, while the contribution of personal goods consumption to GDP growth has fallen to zero. This stands in stark contrast to the late 1990s Internet boom, when a large share of new investment went to labor income, substantially lifting household earnings and driving rapid consumption growth. As shown in the right chart of Figure 1: during the Internet boom, U.S. GDP growth and personal consumption remained strong. But after the bubble burst in 2000, growth in personal income slowed, dragging down both economic expansion and consumption momentum simultaneously.

Source: Bloomberg, CEIC, Wind

Fourth, precisely due to the factors outlined in the third point above, the late-1990s internet boom effectively boosted household income and employment in the US, which in turn drove consumption growth. However, profits of internet businesses failed to improve, leaving shareholders with little earnings returns and ultimately pricking the stock market bubble. By contrast, the current wave of AI investment flows largely into capital goods, energy and other related sectors. In essence, most investment gains remain within the corporate/shareholder sector or are converted into fixed assets, with only a minimal share going toward labor income. This capital allocation model bears strong similarities to China’s large-scale infrastructure and real estate investment drive in 2010s. The outcomes are also comparable: investment concentrates on capital goods sectors — represented by chips, memory and optical modules in this AI cycle, and by non-ferrous metals, coal and heavy machinery during China’s previous infrastructure cycles — delivering leaping revenue growth for these capital goods, while overall household consumption growth downstream remains relatively sluggish. From a profit perspective, the current profit cycle of AI hardware closely resembles that of China’s cyclical sectors. Its sustainability hinges entirely on the ability of core investors to secure continuous financing and scale up capex. In the AI space, this refers to leading large cloud service providers such as Google, Microsoft and Amazon, which are analogous to China’s past infrastructure investment entities including local governments and property developers. As long as the capital chains of these key investors remain intact and they continue ramping up capex and expansion, the stock rally in the hardware cyclical sectors can persist. Conversely, once the market perceives a slowdown in capex growth among major investors, stock price in these cyclical industries will start to decline even if current earnings remain strong. At present, the market is in a peak phase of aggressive upward revisions to earnings forecasts for AI-related stocks. Starting in March, as Q1 earnings reports were released, the upward revisions to US equity forward earnings for 2026 has hit a record high (Figure 2). Total earnings of S&P 500 companies were $2.28 trillion in 2025. The market’s consensus earnings forecast for 2026 has now been revised up to $3 trillion. That means if realized, S&P 500 earnings would surge by more than 30% in 2026, outpacing the cumulative earnings growth recorded over past four-year period from 2022 to 2025 combined. The total market capitalization of the S&P 500 currently stands at $65.6 trillion, implying a forward price-to-earnings ratio of around 22 times.

Source: Bloomberg, CEIC, Wind

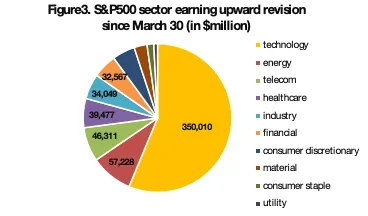

In terms of the magnitude of earnings revision across sectors (Figure 3), the tech sector stands out. Of the total $620 billion upward revision to the S&P 500’s one-year forward earnings expectations, the technology sector contributed $350 billion alone. The second-ranked energy sector’s earnings revision is mainly driven by the sharp rally in oil prices recently. The third-ranked telecom sector is boosted chiefly by two major US AI-related tech giants — Google and Meta — which are categorized within the telecom sector. Meanwhile, consumer discretionary and consumer staple stocks rank down the bottom. This also reflects that market analysts do not believe AI investment can drive a recovery in consumption.

Source: Bloomberg, CEIC, Wind

II.AI drives accelerating K-shaped divergence and surging corporate financing demand

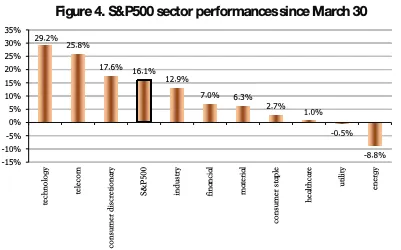

As mentioned above, the rise of the internet in the 1990s differed fundamentally from the current AI boom: back then, most investment translated into household income, driving broad-based consumption growth and expansion across most industries. By contrast, the current growth in AI investment is entirely concentrated in capex and capital formation within a handful of tech sectors, with barely any meaningful boost to labor compensation. When also factoring in AI’s substitution impact on employment in parts of the service industry, overall household income growth may even slow further in the short term as a result of AI investment. This is taking place against a macro backdrop where K-shaped divergence is already accelerating. We therefore expect AI investment to further speed up this divergence—not only widening the wealth and income gap among individuals, but also amplifying the divide across industries and enterprises. Recent global equity market performance is indeed reflecting this logic of accelerating K-shaped divergence. Since the March 30 low, the S&P 500 has rebounded 16%, while technology stocks have surged nearly 30%, with the Philadelphia Semiconductor Index, a key sub-sector, jumping more than 60%. Gains in the telecom sector were largely driven by Google and Meta, while the consumer discretionary index was led mainly by Amazon. Excluding these AI-linked stocks, the broader market’s upside has been extremely reduced. We calculate that the S&P 500 has added a total of $7.4 trillion in market value since its March 30 trough, and the leading tech giants and semiconductor-related stocks alone account for over $6 trillion of that incremental market cap.

Source: Bloomberg, CEIC, Wind

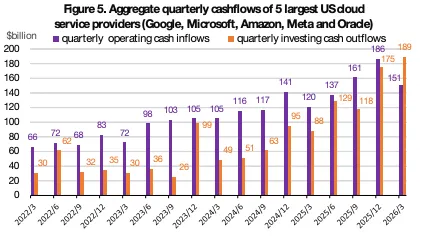

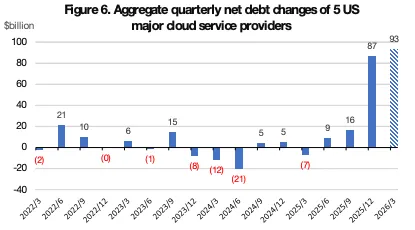

Beyond the K-shaped divergence in the stock market, global investment capital is also accelerating its flow toward AI-related companies. Including equity financing in the PE/VC market, both financing activity and valuation levels for AI-linked firms are rising rapidly. At the same time, facing mounting capex pressure, more leading technology giants have to scale up their financing efforts. For example, AI large model leaders OpenAI and Anthropic both plan to go public as early as this year, and their current market cap have both exceeded $800 billion. In addition, listed large tech giants — especially major cloud service providers facing massive capital spending, mainly the five US firms Google, Microsoft, Amazon, Meta and Oracle — have continuously ramped up corporate bond issuance to raise funds. According to the latest Q1 earnings reports disclosed by these five leading U.S. cloud providers, their combined capex in Q1 reached $188.7 billion, surpassing their aggregate operating cash inflow of $150.7 billion for the same period. In other words, although these companies have seen steady growth in operating cash inflows amid a sharp rise in cloud service income driven by the boom in AI computing power leasing, their capex growth has been even faster. This has instead weakened their cash flow positions, forcing them to expand debt financing to secure additional funding.

Source: Bloomberg, CEIC, Wind

Therefore, we can see that since Q4 last year, the five major US AI cloud service providers have begun to rapidly expand their scale of debt financing. Over the past six months, all five companies have issued substantial amounts of corporate debts, with quarterly net bond issuance proceeds approaching $90 billion. Moreover, to diversify corporate debt market supply pressure, several of these companies have not only issued US dollar-denominated debts, but also raised euro, British sterling and Swiss franc debts in Europe.

Source: Bloomberg, CEIC, Wind

From another perspective, as long as these companies are able to issue debt on a large scale, it means their spending on AI-related capex will continue to expand over the foreseeable one to two quarters ahead. This, in turn, forms the fundamental rationale behind the continuous upward earnings revisions for AI hardware firms. Nevertheless, given the current scale of financing, few companies outside this core group possess the capacity to secure such massive incremental funding on a sustained basis for AI capex. In other words, the pace of overall AI capital spending is largely determined by the investment tempo of these leading firms, and the marginal increase in their investment scale hinges heavily on the scale of their financing expansion. Therefore, for investors allocating to AI hardware stocks such as semiconductors and optical modules, monitoring the financing conditions and funding sustainability of these cloud giants offers a far more reliable gauge for judging future revenue and profit growth across the industry.

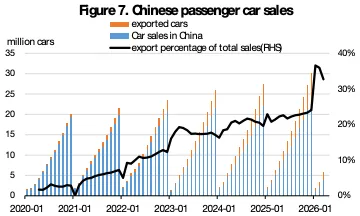

Judging from China’s released Q1 economic data, the domestic economy has continued to maintain the overall pattern of stronger output than consumption, and stronger external demand than domestic demand. Specifically, China’s VAI grew by 6.1% yoy in Q1, while total retail sales of consumer goods rose by merely 2.4% yoy, less than half the growth rate of VAI. As output still outpaces domestic consumption growth, overall economic growth and the balance between supply and demand remain highly reliant on exports. China’s exports surged 14.7% yoy in Q1, marking a further acceleration from last year. Major industries show a similar trend. Take the passenger vehicle industry as an example: a total of 5.93 million passenger vehicles were sold in Q1, down 7.55% yoy. Broken down into domestic sales and exports, domestic passenger vehicle sales were 3.97 million units in Q1, a yoy decline of 22.3%; while exports hit 1.96 million units, a 50% increase from 1.30 million units in Q1 last year. Consequently, passenger vehicle exports accounted for 33% of total sales in Q1, meaning one out of every three passenger vehicles manufactured in China is exported. By comparison, exports only made up 25% of total sales last year.

Source: Bloomberg, CEIC, Wind

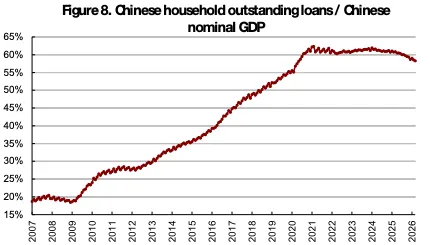

Apart from sluggish household income growth and the drag from reduced consumption subsidies, another key factor weighing on domestic consumption growth is the ongoing trend of household deleveraging in China. At the end of March this year, China’s outstanding household loans stood at 82.7 trillion RMB, down 300 billion RMB from 83 trillion RMB recorded at the end of March 2025. This marks the first yoy net decline in China’s household loan balance over the past two decades. It indicates that the household sector has shifted from stopping leveraging up to actively deleveraging. Over the past few years, the central bank and financial regulators have rolled out a series of measures, including cutting interest rates repeatedly, easing loan approval requirements, lowering the minimum down payment for mortgage, and even exempting minor consumer loan defaults. These policies were all intended to push the household sector back into the leveraging cycle that prevailed before 2021. Nevertheless, the effects have so far remained limited. The ratio of total household loans to GDP is still on a gradual downward trajectory (Figure 8).

From the perspective of stock market investment, as long as Chinese households remain in a deleveraging cycle, stocks in the domestic consumption sector will struggle to stage a genuine and sustained rally.

Source: Bloomberg, CEIC, Wind

IV. Market Strategy

The US-Iran war is drawing to a close. Even if oil prices ease slightly in the short term, previous supply disruptions and inventory drawdowns will keep oil prices elevated for an extended period ahead, thereby continuing to weigh on global consumption. Against this backdrop, stocks closely linked to global retail consumption will continue to suffer from weak demand and elevated energy costs. Global investable capital will keep converging toward AI hardware-related stocks with clear growth prospects, further intensifying the market’s K-shaped divergence. Market indices with high weightings in semiconductors and tech hardware — such as the Nasdaq, South Korean and Taiwan markets, as well as China’s ChiNext Index — are likely to keep advancing. For investors in AI hardware stocks, two key areas require close monitoring: first, the debt financing conditions of large technology firms with massive upcoming capex, particularly the five leading US cloud service providers; second, the growth rate of token usage and procurement among AI large model developers going forward.

US, A-share and Hong Kong stock markets are also likely to maintain K-shaped divergence in the near term. For instance, the Nasdaq will outperform the Dow Jones, while the ChiNext Index will outperform the Shanghai Composite Index. Nevertheless, after the sharp rally over the past month, major market indices are expected to see a slower pace of gains following the pricing-in of positive sentiment from the US-Iran ceasefire.

With market focus rotating back toward AI investment, base metals will have better upside potential than the previously strong energy and chemical sectors. Gold and silver are also set to stage a moderate rebound.

About the Author

·1998 – 2004, Chief Representative Assistant of GKN Group in China.

·2006, obtained an MBA degree from the Wisconsin School of Business at the University of Wisconsin–Madison.

·2006 – 2007, served at the Wisconsin Foundation.

·August 2007 – July 2013, served at China International Capital Corporation (CICC) as the leader of the overseas strategy team and A-share strategy team. He is also the main report writer and contributor. Mr. Hou and his team received many honors including the top team for the New Fortune Sell-side Strategy Research in 2008, and the top team for the Asia Money China Strategy Research in Hong Kong in 2009 and 2012, etc.

·September 2013 – December 2019, served at Discovering Group and was responsible for the Group’s macro strategy research. During this period, the company has accumulated absolute returns that far exceed the market level.

·2020 to present,Chief Strategist of Straits Group.

免责声明:本文件仅供参考。本文件并非作为或在任何情况下被视为对任何资本市场产品的招揽;或购买或出售的要约或要约意图。本文件的内容也不构成对任何人的任何资本市场产品的投资建议。本文件所包含的所有信息均以公开资料为依据,所载资料的来源及观点的出处皆被时瑞集团在发布本文件时认为准确和可靠,但时瑞集团不能保证其准确性或完整性。时瑞集团不对因任何遗漏,错误,不准确,不完整或其他原因而遭受的任何损失或损害(不论是直接,间接或后果性损失或任何其他经济损失)承担任何责任。期货合约、衍生品合约与商品以往的表现或历史数据并不代表未来表现,不应作为日后表现的依据或担保。时瑞集团有权在不通知的情况下随时更改本文件的信息。