夜雨聆风

夜雨聆风本文为《战略定力与战略躁动》的英文版本,增补了部分路演版的内容。

另外,明天是个特别的日子,甚至AI的答题功能都受到了限制。许多年轻小伙、姑娘将会迎来人生中第一次重大考验。

祝他们成功!

First published under the headline *Strategic Resolve and Strategic Restlessness*. The identities of the Strategic Resolve side and the Strategic Restlessness side need no elaboration. March 2026 was defined by two pivotal developments: the crisis in Iran and renewed upheaval in the artificial-intelligence industry led by OpenClaw.

My verdict on Iran is **turbulence fosters resolve**. Put simply, in the Iran standoff, the Strategic Restlessness side has bestowed a decisive strategic gift upon the Strategic Resolve side.

On AI, my reading is ** resolve stirs turbulence**. The Strategic Resolve side is pursuing a gradual, grinding competitive strategy, steadily shrinking the rival’s comfortable terrain in AI industry and pushing it into a corner where impetuosity becomes unavoidable.

Through the lens of China’s traditional yin-yang philosophy, these two dynamics form a circular logic of mutual generation and restraint. Precisely because your restlessness strengthens me, I will cling still more firmly to my resolve—and encourage your further restlessness. Much of today’s global disarray can be grasped through this framework; Iran and AI merely offer the starkest examples.

The oil-price calculus

We begin with the Iran crisis.

China’s trade and investment with the Middle East remain modest. Despite rapid growth in recent years, absolute volumes are still small. The economic impact of Iran’s turmoil on China will therefore be channeled mainly through oil prices, in two distinct ways.

The first is the vanishing of the **Iran discount**. Ironically, this discount exists because of American sanctions.

Under its domestic law, the United States bans all countries around world from trading with Iran, leaving Iranian oil unable to find buyers even at knockdown prices—precisely Washington’s goal. Yet China has defied those sanctions to trade with Iran, securing crude at a discount to international benchmarks. This represents a tangible gain.

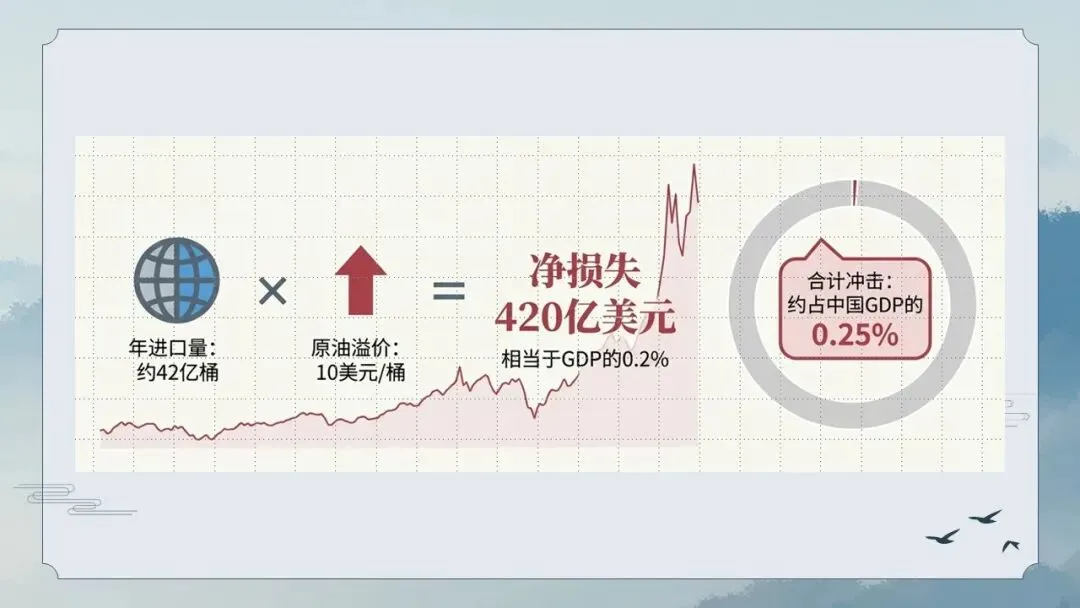

In the absence of official data, we take upper-bound estimates on a prudent basis. China imports no more than 600m barrels of crude from Iran each year, with a maximum discount of $15 per barrel. That puts the annual gain at no more than $9bn—less than 1% of China’s 2025 goods-trade surplus, or roughly 0.05% of its GDP.

If Iran were to lose all oil-export capacity, or if America lifted sanctions unconditionally, the Iran discount—and China’s windfall—would disappear. If Iran’s exports survive and sanctions stay, the benefit endures.

In truth, this discount is the only idiosyncratic effect of the Iran crisis on China. The larger shock comes from rising oil prices—but crude is a global macro variable that hits all economies almost equally. It must be analyzed through macroeconomics, not event-driven storytelling.

Some argue that oil flowing through the Strait of Hormuz has historically headed mainly to East Asia, so the Iran crisis hurts the region most. That is misleading. Global oil prices are tightly integrated: Brent and WTI futures move in lockstep. Wide spreads would trigger arbitrage, since America has not banned its own oil exports.

The upper-bound impact on China’s external balances can be estimated simply. China imports 4.2bn barrels of crude a year; a $10 per barrel rise adds $42bn to its import bill, equivalent to roughly 0.2% of GDP.

Sceptics will note that oil has risen by far more than $10. But headlines quote front-month futures; our annual estimate averages June, September and December contracts, where gains are far more muted. Further price rises would push the cost higher, of course.

All told, the combined direct economic hit to China from a lost discount and higher oil amounts to a few tenths of a percentage point of GDP. The damage is real and meaningful—but far from crippling.

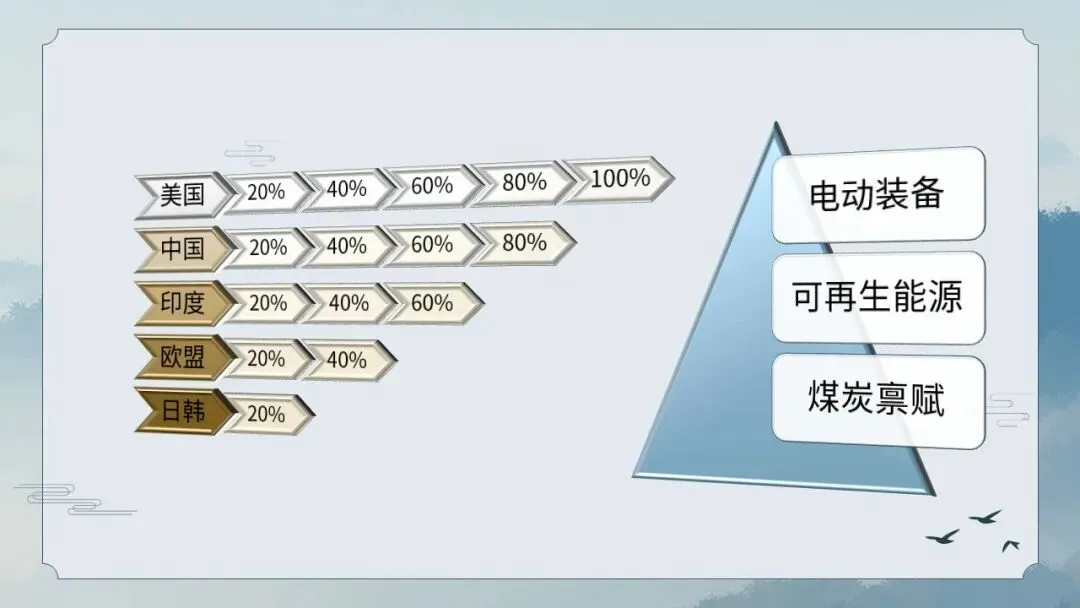

The key measure is **primary energy self-sufficiency**. Less precise than GDP or market capitalization, it is nationally estimated. America stands slightly above 100%, China around 80%, India 60%, the EU 40%, and Japan and South Korea below 20%. That is the unforgiving arithmetic.

Among major economies, China’s energy self-sufficiency is second only to America’s. It rests first on abundant coal reserves in Shanxi and Inner Mongolia. Second comes the breakneck expansion of renewables: solar, wind and hydro. Third, China’s end-use demand is already heavily electrified—electric vehicles, high-speed rail, converter steelmaking and aluminum smelting, to name a few.

A widely cited figure is **days of crude cover**: stocks divided by daily imports. Foreign media put China at just over 100 days, while Japan and South Korea hold nearly 200 days or more. Some conclude that makes Japan and South Korea more resilient. That is dead wrong.

In economic modelling, structure matters more than numbers. China’s 80% self-sufficiency means imports fill only a 20% gap. In a crisis, other energy sources, pipeline flows and demand restraint can shrink that gap to 10%—turning 100 days of cover into 200. Even 400 days or virtually unlimited is possible if necessary.

For Japan and South Korea, with self-sufficiency below 20%, no such buffer exists. In a crisis, they absorb the full shock; once their 200 days run out, social and economic breakdown looms. Their resilience is not in the same league as China’s.

Such is the energy-supply calculus.

America is more than 100% energy self-sufficient, so oil prices seem to matter little for the economy as a whole. But domestically, higher oil redistributes massive income from consumers to oil giants, reshaping spending patterns and indirectly weighing on consumption, GDP and macro stability.

On a deeper level, rising oil will widen inequality and sharpen America’s social divisions. Midterm elections loom late this year; a Democratic-controlled Congress could move towards impeachment. Donald Trump’s claim that he cares nothing about higher oil prices is cynical rhetoric for his MAGA base.

Since the COVID-19 crisis, inflation in America and Europe has stayed stubbornly high, failing to return to target. China, by contrast, has teetered on the edge of deflation for years. A modest externally driven rise in inflation might, in that light, be welcome.

Higher oil does not improve China’s overall welfare—it merely redistributes income. Net debtors, including firms and mortgage holders, stand to gain. Losers are holders of fixed-income assets, such as investors who bought 10-year government bonds at yields of 1.5% and 1.6%.

Such is the macroeconomic view.

Should geopolitical frictions in Iran spiral deeper, or even if governments broker an official cross-border ceasefire, endemic civil unrest, population displacement and militant violence could still gnaw away at global economic stability. The world may then find itself retracing the macroeconomic script of the 1970s.

Wars in the Middle East and cascading oil crises half a century ago unleashed stagflation across the globe. In that environment, Japan’s small, economical cars swiftly came to dominate global consumer markets.

In the language of economics, stagflation disproportionately rewards goods with low income-elasticity: affordable, reliable necessities for household spending. Applying that pattern to the present era, a repeat spell of stagflation in the 2020s would hand a distinct structural advantage to products stamped Made in China.

Such is the trajectory unfolding across global industrial dynamics.

Energy Autarky

Beyond the analytical lenses used so far, one momentous shift stands out: the **fundamental reordering of the pricing logic** for the new-energy industry.

For years, judging renewables has boiled down to microeconomic factors—efficiency, costs, and at best, a superficial nod to environmentalism. What has long been excluded from valuation is a defining strategic virtue: **energy autarky**. The recent crisis in Iran has laid this bare.

Micro factors translate into fixed numbers; a 5% gap is just a 5% gap. Strategic value, by contrast, is elastic. As a Chinese proverb puts it: “Off the scales, it weighs nothing; on the scales, it outweighs a thousand catties.” When strategic value imperatives kick in, marginal micro differences become irrelevant.

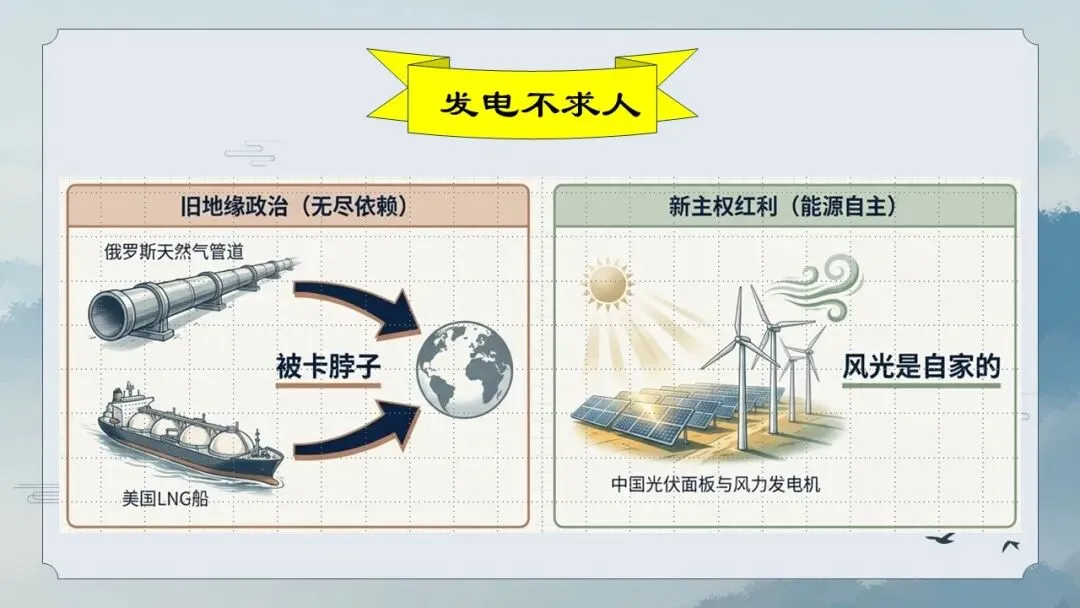

Take Europe’s dilemma. Long dependent on Russian pipeline oil and gas, it now seeks to pivot to American LNG. In truth, both routes leave it exposed to supply coercion. If Russia does not weaponize energy, the United States will.

Which country would not hold Europe to ransom? China. Buy Chinese solar panels and wind turbines, and the wind and sun are Europe’s own. China cannot cut that off, even if it wished to. That is **energy autarky**.

Coal has been used for millennia; the oil industry has matured over a century. Yet large-scale renewable deployment spans little more than a decade. China’s National Bureau of Statistics only added a dedicated “solar power” series in 2014.

As another proverb notes: “Time reveals a horse’s strength; adversity reveals one’s character.” Humanity’s understanding of renewables remains deeply incomplete. No one has properly priced the principle of **energy autarky**. Practice will reveal its true value.

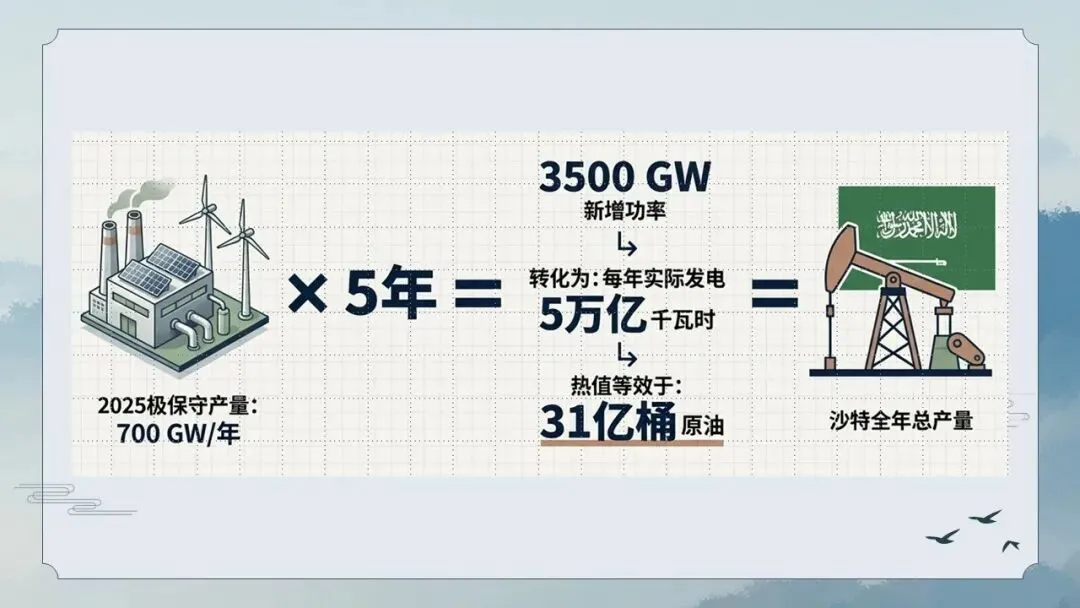

To quantify the scale: China’s combined solar and wind manufacturing capacity—for domestic installation and exports—has reached a conservative 700 gigawatts (GW) in 2025. Over five years, that totals 3,500 GW. How much electricity can that yield?

Using a simplified composite coefficient that incorporates grid balancing, asset mix and conversion efficiency: China’s 1,800 GW of installed solar and wind capacity is projected to generate roughly 2.3trn kilowatt-hours (kWh) in 2025. That ratio provides a benchmark.

On this basis, 3,500 GW of capacity could generate roughly 5trn kWh a year—equivalent in energy terms to 3.1bn barrels of crude oil. That is roughly Saudi Arabia’s annual output.

In short, China can build the energy equivalent of one Saudi Arabia every five years. A decade would deliver two; 15 years, three. With urgency, one every three years and four in a decade is plausible.

Consider the turnaround: in 2016, solar power was barely visible in official data. By 2026, China can build a Saudi-scale clean-energy equivalent in half a decade. Such is the speed of transformation.

A new energy order is emerging—one that can challenge the entire fossil-fuel establishment on equal terms.

Against this backdrop, obsessing over short-term oil-price moves during the Iran crisis looks parochial. The key trend is clear: **any turmoil in the fossil-fuel world strengthens renewables—and thus benefits China.** China’s position in the new-energy pecking order will surpass OPEC at its peak.

Some readers still crave a military verdict: who wins, who loses? On military details, I have no privileged information. But I have a methodological edge: history. Iraq and Afghanistan were devastated by American intervention. Yet even in defeat, did U.S. win? Few Americans would agree.

War is not a zero-sum game; it can produce mutual losers. From the first day of fighting, U.S. and Iran were set to lose together. The only winner of fossil-fuel infighting is renewables.

This analysis makes plain that an attack on Iran would be a strategic blunder born of Washington’s strategic restlessness. Where, then, does China’s strategic resolve shine through? Was its renewable push just a lucky break?

To answer that, we must take a higher view to see the full strategic landscape.

The Post-2008 Crisis Era

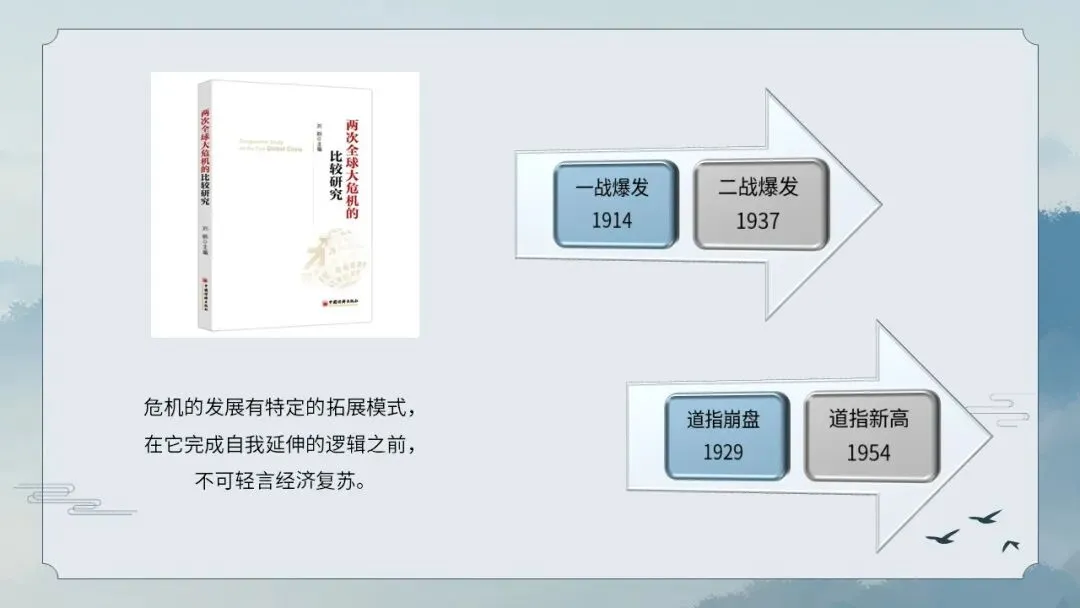

Here I recommend a book I hold in high regard: *Comparative Studies of Two Global Crises*, edited by Liu He, former Vice Premier of the People’s Republic of China. It contains a well-known maxim: **A crisis evolves along a set logic of expansion; one ought not to declare an economic recovery prematurely before it runs its full course. **

The book was widely followed in stock market circle ahead of the 2015 and 2016 market events. Yet as time passes, it has gradually faded from memory. Many professionals today were probably in college or even high school in 2008. That great crisis is indeed some years behind us.

Still, I wish to highlight two stark facts. First: World War I broke out in 1914 and World War II in 1937, a gap of 23 years. Second: The Dow Jones Industrial Average collapsed in 1929 and did not regain its peak until 1954, a span of 25 years.

After World War I, John Maynard Keynes wrote his seminal work *The Economic Consequences of the Peace*. He argued that the Great War had failed to resolve the fundamental contradictions behind global instability, and that tensions would resurface sooner or later. That “sooner or later” spanned 23 years.

The 1929 Dow crash paved the way for Franklin D. Roosevelt’s New Deal, followed by America’s entry into World War II. The Bretton Woods system was established in 1944. By the end of the war in 1945, the United States accounted for more than half of global industrial output and gold reserves, enjoying unrivalled economic dominance. Yet the Dow had not recovered its pre-crisis levels. It took a further nine years—25 years in total—to climb out of the abyss of the Great Depression.

Human life is fleeting. How many 25-year cycles can one lifetime contain? Yet we must recognize that shifts in the global order unfold at a glacial pace. For the sweep of global history, 25 years is but a blink. When people look back on 2026 decades or centuries from now, how will they characterize this era? I believe they will define it as the **post-2008 crisis era**.

The logic is straightforward. Until a Third World War erupts, we remain anchored in the post-WWII order. And until a sufficiently transformative landmark event occurs, we will continue to live in the shadow of the post-2008 crisis era.

The defining feature of the post-2008 crisis era? **Deglobalization**. The regions where deglobalization bites deepest are known as the **Rust Belt**.

The concept of Rust Belt entered widespread public consciousness largely thanks to Donald Trump’s unexpected rise in American politics. It describes regions left behind by globalization. Their residents enjoyed prosperity three or four decades ago, but their absolute living standards have stagnated while their relative position has declined, leaving them feeling abandoned by globalization. These voters are the most disillusioned, demand the most radical change, and thus elected a most disruptive president.

If we substitute “residents” with “nations”, I would argue that there is also a Rust Belt on the world map: Eastern Europe and the Middle East. Forty years ago, when China had just launched reform and opening-up, a Chinese person who visited Budapest, Beirut or Damascus could boast about it for years. Yet after the high-growth phase of globalization, their absolute economic progress has been modest, and they have been overtaken by East Asia in relative terms—an exact parallel to the American Rust Belt.

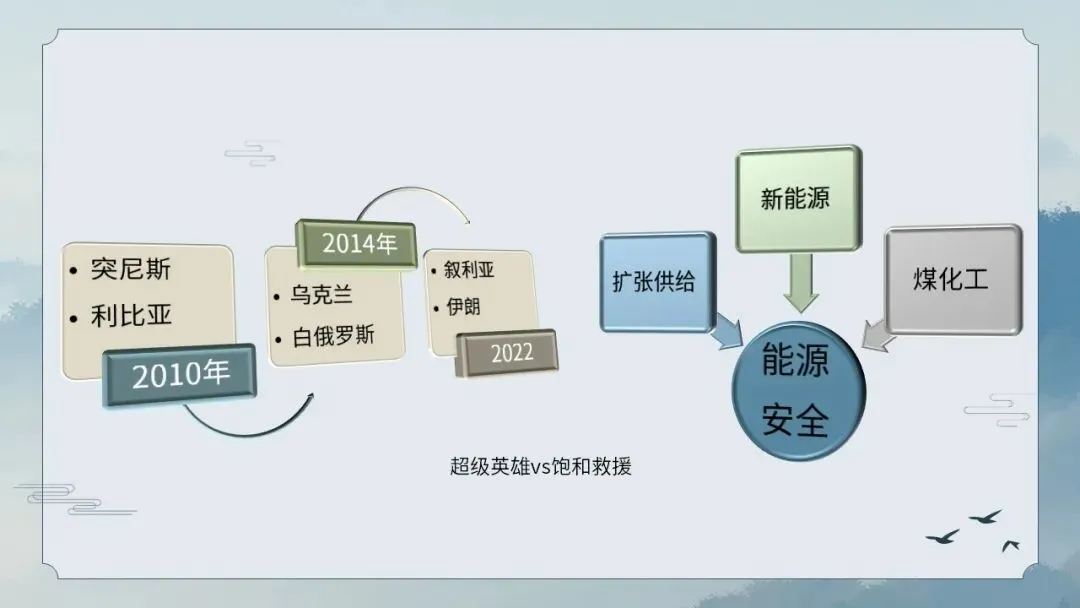

As an ancient Chinese proverb observes: **Where there is injustice, there is outcry.** Where resentment festers, disruption follows. In 2010, unrest erupted first in Tunisia, then spread to Libya and Egypt. Their regimes fell in what became known as the Arab Spring. Strategic analysts at the time widely predicted the turmoil would roll eastwards, engulfing Syria, Jordan, Saudi Arabia and ultimately Iran.

That scenario never materialized. After the 2008 crisis, China launched its RMB 4tn stimulus package, which boosted crude oil demand. The Arab Spring thus sent oil prices surging, shoring up the fiscal positions of Gulf oil producers, who could buy social stability.

Curiously, the wave of social change did not cross the Red Sea into the Arabian Peninsula, but instead crossed the eastern Mediterranean into the Balkans. Color revolutions followed in Bulgaria, Serbia, Ukraine and Belarus. Russia itself teetered on instability. Then came the Crimean referendum, the Donbas crisis in eastern Ukraine, and finally the outbreak of the Russia-Ukraine conflict in 2022.

The war drained Russia’s resources, leaving its Middle Eastern proxy—the Assad regime in Syria—unable to hold on and collapse. A major rupture opened in the so-called Shia Crescent. Israel, citing counter-terrorism, launched an all-out war against Shia-led governments. After more than a decade of twists and turns, the flames of conflict have finally reached Iran.

While we sympathies with war victims on humanitarian grounds, we must acknowledge that a failed national strategy, despair among ordinary people, elite disenchantment and civil society deeply infiltrated by foreign forces all leave a country vulnerable to external intervention. In the end, Iran could not escape the fate of the global Rust Belt.

The above narrative unfolds geographically. Viewed chronologically, a striking pattern emerges when cross-referenced with crude oil price charts: **When oil prices are high, Iranian tensions ease; when prices fall, they escalate.**

In 2010, oil traded below $80 a barrel, and the Arab Spring erupted. Prices quickly surged above $120, filling oil exporters’ coffers. The Obama administration then led negotiations over the Iran nuclear deal (JCPOA). Next, a breakthrough in US shale oil and gas technology pushed prices down to around $60. In 2018, Trump withdrew from the JCPOA, and US-Iran tensions flared. The 2022 Russia-Ukraine war sent oil back above $120, temporarily defusing US-Iran frictions. Then widespread adoption of Chinese new energy technologies pushed prices below $80 again. In March 2026, the current Iran crisis erupted.

In short, the outbreak of the Iran crisis was historically inevitable, both geographically and chronologically. When we step back and set aside trivial details, the central narrative stands clear. As a classical Chinese poem puts it: **We fail to see the true face of Mount Lu because we are standing right in the middle of it.**

Many people claim to devote enormous effort to research, yet they merely fixate on minute-by-minute headlines, absorbing information without reflection. CNN dubs these people **news consumers**. Studies suggest that their brain activity when following the news resembles that of watching a film, rather than studying or taking an exam.

Readers may still ask: Why does the United States insist on targeting Iran? It is a complex question, with answers spanning religion, economics, geopolitics and ideology. Yet I prefer Occam’s Razor: if a matter can be explained in one sentence, do not overcomplicate it.

What is that sentence? The *Records of the Warring States* records a dialogue between Lv Buwei and his father.

Lv Buwei: What is the return from farming?

Father: Tenfold.

Lv Buwei: What is the return from trading pearls and jade?

Father: A hundredfold.

Lv Buwei: What is the return from installing a ruler of a state?

Father: Incalculable.

Such was the plain wisdom of the ancients 2,000 years ago. Today, China advocates peaceful coexistence and a community with a shared future for mankind. Many have thus forgotten the practice of “installing a state ruler”. But imperialism never forgot.

Aristotle wrote: **Nature abhors a vacuum. ** Imperialism abhors independence. Any nation that seeks sovereignty and self-determination is intolerable to imperialism, which will stop at nothing to remove it. That is my concise answer to why the United States stirs unrest across the world.

Overt Stratagem

We spend far more time analyzing China’s macroeconomy than the global strategy. Yet even then, we often miss the bigger picture too. Look closely, and many Chinese policies appear messy, iterative and tentative—hardly the work of an all-knowing, infallible state.

Foreign observers, by contrast, often see something else. From a distance, they detect a deliberate, long-term **Overt Stratagem** that China has pursued across sectors for decades.

Take energy security. After the 2008 crisis, unrest in the Middle East posed a persistent threat to crude supplies. Spotting that risk was not hard. The real test was what to do about it.

Sixteen years separate the Arab Spring of 2010 from the Iran events of 2026. For individuals, that is a lifetime. For the global order, it is a blink. Iran, for one, achieved almost nothing in that period to alter its strategic predicament.

History offers a parallel. After the 1929 Depression, China’s Republic enjoyed a “Golden Decade” of growth as silver weakened against gold. Yet it changed nothing. From the first Sino‑Japanese war to the Twenty‑One Demands, from the Mukden Incident to the Marco Polo Bridge clash, China remained strategically trapped by Japan.

This time, post‑2008, China has engineered an industrial miracle. Without it, Middle East turmoil would have hit its economy far harder.

That miracle rests on three pillars. First is the push into new energy, already discussed. Second is massive supply expansion. Too many see energy security through the lens of trading: buy low, sell high, like stocks.

That works for small economies—Japan, South Korea, India. Microeconomics teaches: small producers are price‑takers; big producers are price‑setters. China uses as much energy as America, Europe, Japan and South Korea combined. It should not depend on trading; it **sets terms**.

How? By expanding supply to depress prices. Central Asian oil and gas, far from ports, became viable via pipelines from Xinjiang to Shanghai. The Belt and Road Initiative’s global infrastructure drive is, at its core, a push to expand supply and cap prices. So too is China’s commitment to multilateralism and peace.

Third is coal chemistry. Earlier we teased the idea of “building a Saudi Arabia in five years”. Oil provides both energy and chemical feedstocks: carbon and hydrogen. But it is not irreplaceable. Carbon can come from coal; hydrogen from water. The technology works; only cost varies.

Commercially, coal chemistry is awkward: often feasible at market prices, but loss‑making. Yet China has invested for decades and now leads the world technologically. That tells its own story.

Hollywood superhero films suggest one savior fixes everything. China’s energy strategy is closer to the “saturation rescue” in *The Wandering Earth*: if one line fails, another takes its place.

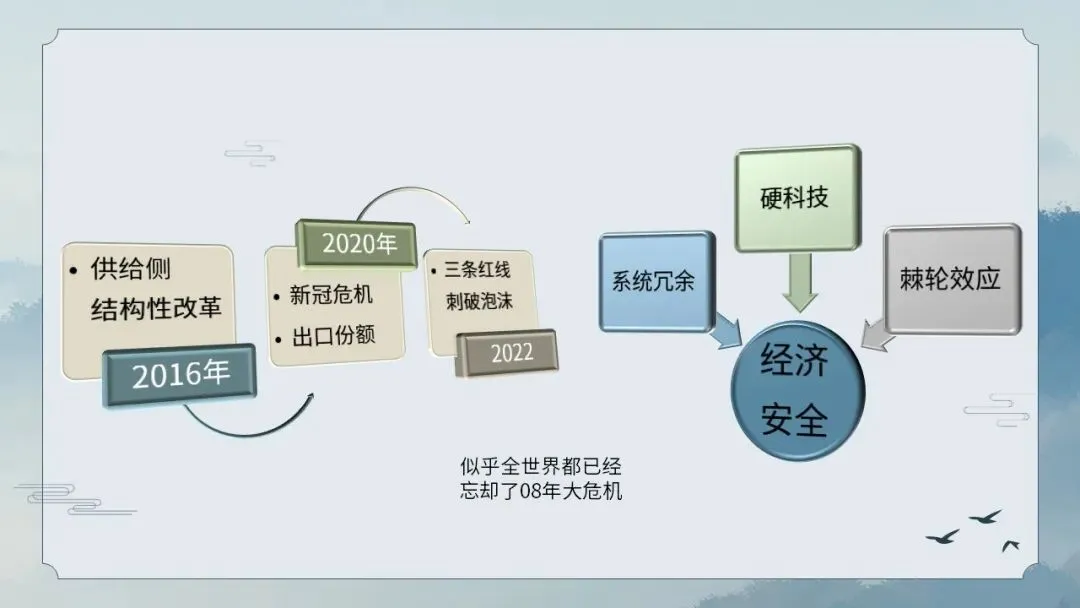

Zoom out, and a similar Overt Stratagem defines China’s macroeconomic policy. The 2016 supply‑side reforms, the 2020 export surge during COVID, the 2022 “Three Red Lines” to deflate the property bubble—one word binds them all: **economic security**.

This, too, has three pillars. First is **systemic redundancy**: not cut‑throat downstream competition, but robust upstream resource guarantees. The 2016 reforms targeted coal, steel and non‑ferrous metals.

Less noticed by markets but stressed by state media is “grain stored in land, grain stored in technology”. Foreign reports say China holds more than half the world’s grain reserves—a trivial detail in calm times, a decisive advantage in crisis. Famine alone reveals grain’s true price.

Fiscal and monetary space are also forms of redundancy. Since COVID, deficits have surged across major economies. China has held back. Under the Constitution, its government has far more borrowing capacity than Western peers; it simply keeps it in reserve.

Second is **hard technology**. China has never let up in pursuing new quality productive forces. The reason is age‑old: as Deng Xiaoping put it over 30 years ago, **lag behind and you get bullied**.

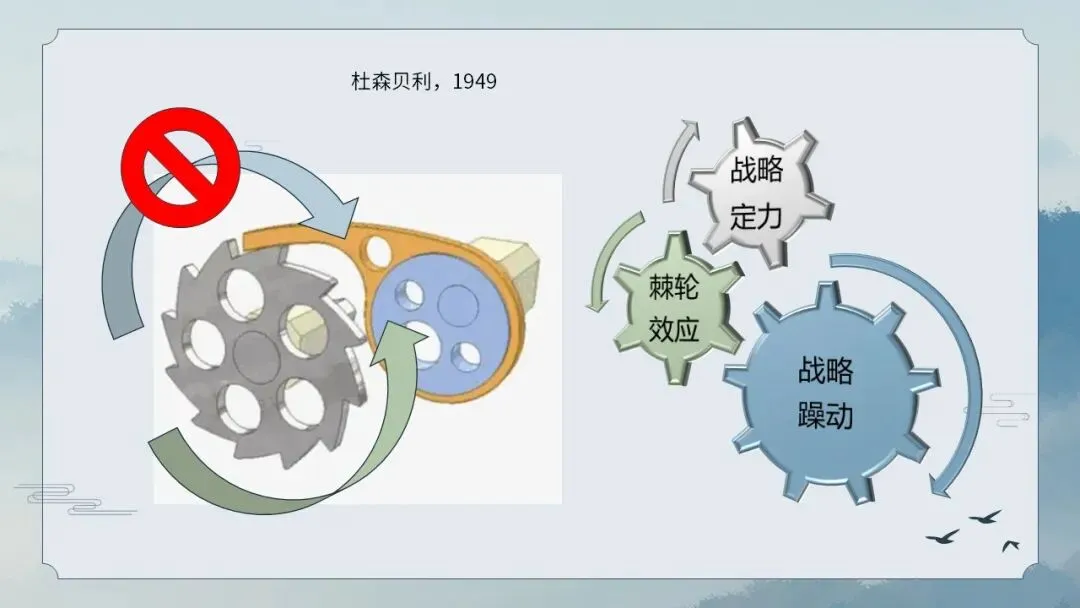

Third is the **ratchet effect**, named by economist James Duesenberry in 1949. Consumption rises with income but does not fall when income drops. As a Chinese proverb puts it: “From frugality to luxury is easy; from luxury to frugality is hard.”

This explains China’s and America’s differing paths. China is at the bottom of the welfare ratchet. Raising benefits prematurely and unsustainably would bring more pain from their loss than joy from their gain. The greater the external risk, the more cautious China is.

America sits at the top. Extra benefits bring little joy; cutting them brings acute pain. It will resist correction by any means. Economies move in cycles: boom and cooling, expansion and adjustment. Yet Americans cannot accept even normal downturns.

China’s rise makes this rigidity worse. After the dotcom crash, America could tolerate adjustment: its dominance was unchallenged. Today, China’s all‑round catch‑up makes any retreat unbearable.

China understands this. Its only logical choice is its Overt Stratagem: the more restless America’s strategy becomes, the more resolve China remains—meeting constant chaos with unshakable stability.

Hence the logic: **turbulence fosters resolve; resolve stirs turbulence**—two strategies locked in mutual opposition.

Macro Recklessness

We turn now to the United States. In recent years the country has been racked by deep social and political dysfunction, a breakdown plain for all the world to observe. Yet capital markets remain split over whether such turmoil should be priced into asset values.

The long‑standing consensus among investors was that such disturbances ought not to move prices, a view rooted in headline macroeconomic indicators: GDP, unemployment, corporate profits. By these measures the American economy looks robust, its growth strong, with little cause for alarm.

But since Donald Trump returned to office in 2025, his agenda has forced a rethink among market participants, who now grapple with how to price policy risk. Any credible assessment must answer two questions: first, whether these risks are material; second, whether they are systemic.

Start with materiality. Mr. Trump’s style is notorious. So, U.S. domestic debate fixates on his personality; global attention on his foreign policy. The domestic economic impact of his rule has been largely overlooked. Three areas stand out.

First, electric vehicles. The car industry is a pillar of American manufacturing. Mr. Trump has torn up long‑standing policies for electrification. Struggling carmakers have abandoned EV projects wholesale, triggering tens of billions of dollars in write‑downs, model cancellations, factory closures and job losses. Even a change of administration will not undo the damage. In truth, America may have closed its final window to lead the global EV transition.

Second, university research. The Trump administration has targeted world‑leading institutions such as Harvard and Columbia, slashing research funding. For decades university research has underpinned America’s technological hegemony. Even before Mr. Trump, funding had grown scarce after the 2008 financial crisis. The recent crackdown has left American universities far less attractive; researchers now leave faster than they arrive.

Third, bank capital. This policy, in our view, most clearly reveals the worldview of Mr. Trump’s Make America Great Again supporters. His attempts to influence the Federal Reserve are well‑noted, yet attention focuses on chairmanship choices and interest‑rate cuts. A 25 or 50 basis‑point cut in the federal funds rate matters little to the real economy. Far more important is Michelle Bowman, the vice‑chair for supervision, who has led a sweeping deregulatory push—centered on looser bank capital requirements.

The global regulatory norm, enshrined in the Basel Accords, is countercyclical macroprudential policy: tighten capital rules when the economy booms, loosen them when it weakens. The logic is simple: save in good times to spend in bad.

America is now doing the opposite: pursuing procyclical macro recklessness. It seeks to stoke faster growth when the economy is already strong, pouring fuel on the fire, as if trees could grow endlessly skyward. When the bubble bursts and the cycle turns, what ammunition will remain? The MAGA base shows little interest in such questions.

These three examples make plain that the Trump administration is far more than a sideshow. Its policies are hollowing out the foundations of the American economy. Most effects are indirect, yet the damage could emerge sooner than many think. These risks are undeniably material.

Is the risk also systemic? Many observers still blame Mr. Trump as an individual, assuming that once he leaves office—or changes his mind—normality will return. This view is dangerously complacent. Events will keep exceeding such expectations.

In a direct presidential system, the bond between voters and president resembles that between fund investors and managers. Investors choose when and what kind of fund to put money into; managers trade within their mandate. If investors pour into aggressive funds at market peaks and lose money, both sides are at fault—not just one.

Mr. Trump’s rule has been mocked as “wrecking‑ball governance”. Yet it is American voters who have twice put him in office.

When Barack Obama took office in 2008, his rallying cry was “Change”. Today that sentiment has curdled into resentment of the status quo. Choices are no longer about rational calculation but desperate gambles.

Mr. Trump did not appear out of nowhere. He is the product of this national mood—a perverse “effectiveness” of America’s electoral system.

Even a change of government will not bring calm. A new administration must still answer an angry public; only the targets will differ. A Democratic government would probably push sharp tax rises and heavy regulation, equally punishing to capital returns. Silicon Valley bosses’ early embrace of Mr. Trump reflected just such a calculation.

Why does the American economy look strong on headline data yet stir such popular anger? The answer lies in both objective and subjective forces.

Objectively, inequality has reached extreme levels. Stories of homeless people’s hardships have resonated widely in China.

Yet this picture is incomplete. America is a country of over 300m people. The poorest 10% number 30m; the poorest 20% 60m. Not all are homeless.

Official Fed data show roughly half of Americans have no net worth, living paycheck to paycheck. But as long as they remain employed, their living standards hold up. One must not equate ordinary Americans’ lives with those in parts of Latin America, South Asia or Africa.

Then we need subjective explanations. Among them, the ratchet effect is powerful. Most of today’s American middle class lived through the post-Cold War zenith of national prosperity. After 2008 the tide receded, but the myth of the American Dream lived on. They regard 12‑month bonuses, 15% annual pension growth, $150,000 blue‑collar jobs and unicorn start‑ups within two years as normal entitlements. Extremes of expectation breed resentment.

One revealing detail: months before formal nomination, Mr. Trump named Kevin Walsh as his choice for Fed chairman. In a Fox News interview, he claimed that under Mr. Walsh growth could hit 15%. The remark gained little coverage, perhaps because it defies credibility. A 15% growth rate for U.S. is all but unimaginable.

Yet nominal GDP growth tells a striking story: 10.5% in 2021, 9.2% in 2022, 5.7% in 2023—all extremely high.

Serious economists rightly note these figures are inflated by inflation. Real growth has hovered between 2% and 3%, even after massive post‑pandemic stimulus.

This technical point is valid. But only economists care about real growth. Stock prices, enterprise profits, house prices, wages and bonuses are all nominal. The 15% growth the MAGA base craves is also nominal growth.

These lays bare the psychology: they reject inflation but demand high nominal growth—in effect, wanting fantasy to become reality. Reasonable or not, politicians are under pressure to deliver by gamble.

Is procyclical macro recklessness a systemic risk that markets must price in? It is a question Wall Street can no longer ignore.

A World Out of Balance

I recommend a seminal work: *The Alchemy of Finance* by financier George Soros, where he first articulated the concept of reflexivity.

In a speech in May 2023, *On VFCC, a Macro View*, I applied Soros’s framework to draw a parallel between America today and the United States of the early 1980s—a comparison that clarifies many puzzling trends. Soros dubbed that era the Reagan Imperial Cycle; by extension, we now live in what can be called the Trump Imperial Cycle. The full logic is complex, and I shall not retrace it here.

In June 2025, I delivered another speech, *When Whale Falls, Others Thrive*. There I simplified the Reagan Imperial Cycle and highlighted its three most glaring bubbles: the bubble in US equity valuations, the bubble in US dollar purchasing power, and the bubble in discretionary spending within US GDP. This is my **Triple Bubble Thesis**.

Today I simplify still further, focusing on just one pivotal measure: GDP. I set aside China and examine only the other three largest economic blocs—the United States, the European Union and Japan. I use no adjusted figures, only official statistics, laying out facts plain for all to judge.

Between 2005 and 2025, 20‑year **real GDP growth** reached 42% in the U.S., 20% in the EU and 12% in Japan. America led, Japan lagged—a familiar hierarchy, yet the gaps were moderate.

In **nominal GDP**, the U.S. rose 104%, the EU 64% and Japan just 28%. Inflation stretched the divergence considerably.

Yet the most striking contrast is in **dollar‑denominated GDP**: the U.S. up 104%, the EU a mere 31%, and Japan **down 23%**.

U.S. has higher inflation and a weaker dollar in purchasing‑power terms, yet the currency has strengthened. How can this paradox persist? Can the rift between the dollar’s exchange rate and its real value widen forever? If equilibrium is to reassert itself, how will it happen—and what will trigger it? These questions matter to everyone.

Today we focus only on GDP. If this piques interest, you may revisit my earlier speeches. Better still, read Soros in full; the intellectual originality is his.

Soros’s underlying worldview also bears emphasis. Mainstream economics starts from the assumption of equilibrium. Soros insists equilibrium is unattainable. The economy oscillates like a sine wave around a neutral axis but never settles there. In short, the economy is either overheating, cooling, or moving toward one of them—**equilibrium is never a stable state**.

The appeal of equilibrium is that it simplifies analysis. When a shock occurs, we can study it in isolation rather than tracing its ripple effects across time and space. That’s how CNN feeds your brain with fleeting news headlines. Yet the real world, I argue, conforms far better to Soros’s insight: there is no such thing.

As a Chinese proverb observes: *The tree wishes to stand still, but the wind does not cease.* We never face a single, isolated event. We face an interconnected world and its whole history, where every seemingly separate incident is merely one expression of this organic system at a given time and place.

To see only trees, not the forest, is to act in a piecemeal, reactive way. The result will be constant scrambling, trapped between advance and retreat.

Seen this way, the 2008 financial crisis demands re‑examination. Much of the post‑2008 crisis prosperity has rested on America’s triple bubbles. So we must ask: Can American companies permanently dominate the world’s frontier technologies? Can the U.S. economy sustain vast structural trade deficits indefinitely? Do the dollars earned through hard work by countries around the globe hold genuine value?

I do not aim to answer these questions here; I only pose them for reflection. For it is only when the tide goes out that you find out who is swimming naked.

Trapped on the Tiger’s Back

If there is one risk most likely to precipitate a collapse in America’s current economic cycle, it is the bursting of the artificial intelligence bubble. On this count, financial markets are in rare accord. What follows assesses the latest shifts in the AI industry and the logic of what I call **resolve stirs turbulence**.

I contend that America’s AI sector is now **trapped on the tiger’s back**—a predicament with two facets: why it climbed aboard, and why it cannot dismount.

As these arguments have been aired before, I draw directly on past speeches for brevity. In January 2025, in *Facing and Breaking The Wall*, I wrote:

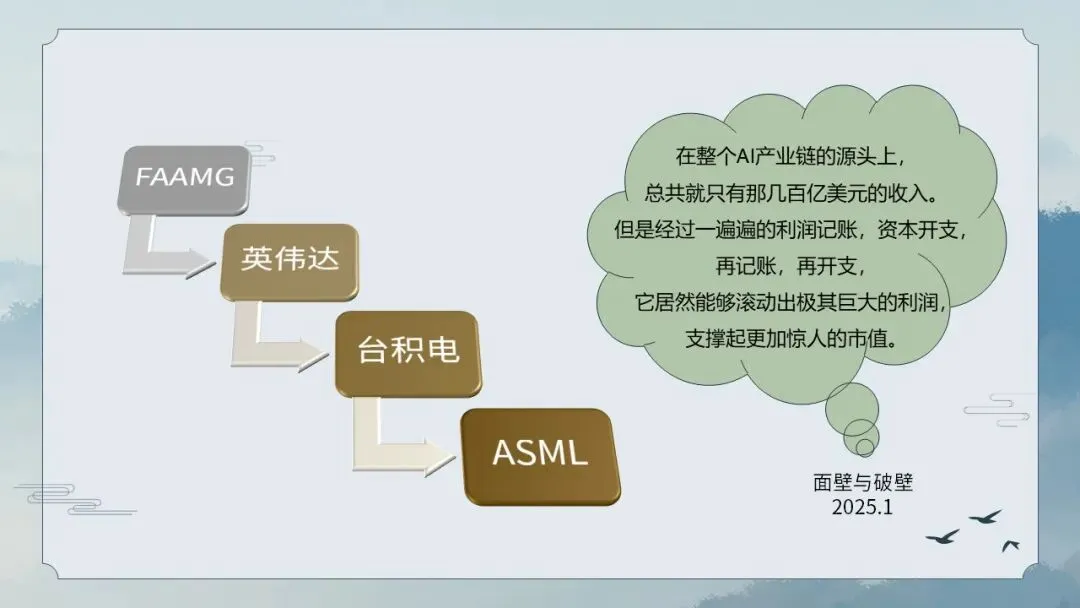

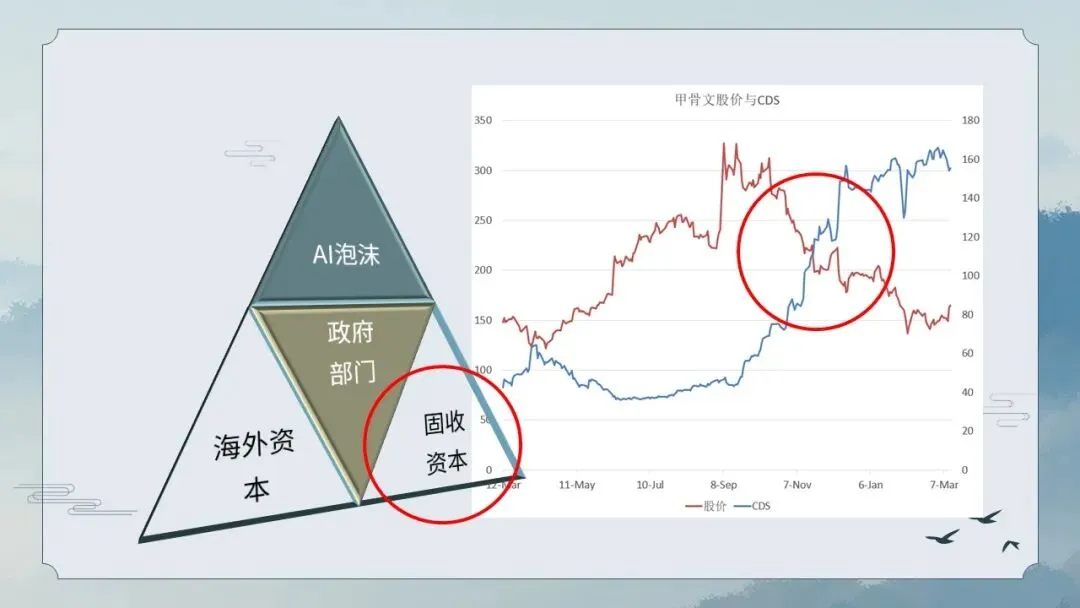

At the source of the entire AI industry lies just a few tens of billions of dollars in revenue. Yet through successive rounds of profit booking, capital expenditure, rebooking and reinvestment, this modest base has been magnified into extraordinary profits, underpinning still more eye‑watering market valuations.

To put it simply: under accounting principles, entities under common control should consolidate their financial statements. Capital expenditure has a peculiarity: it is not recorded as a cost by Firm A, yet can become revenue and profit for Firm B. Groups of companies bound by tight, material shared interests can readily collude to inflate profits by exploiting this loophole.

The top tier of the AI industry can be counted on one hand, bound by thick capital and business ties. Admittedly, under current rules, proving common control is difficult. Yet regulation evolves only in the aftermath of crisis. It took the implosion of the dotcom bubble to lay bare Enron’s engineered trades in natural gas futures. So in the unfolding AI bubble, malpractice is all but inevitable—a product of human nature. **Caveat emptor**.

That explains why the industry is like riding a tiger. Now for why dismounting is impossible. In December 2025, in *Equilibrium and Margins*, I observed:

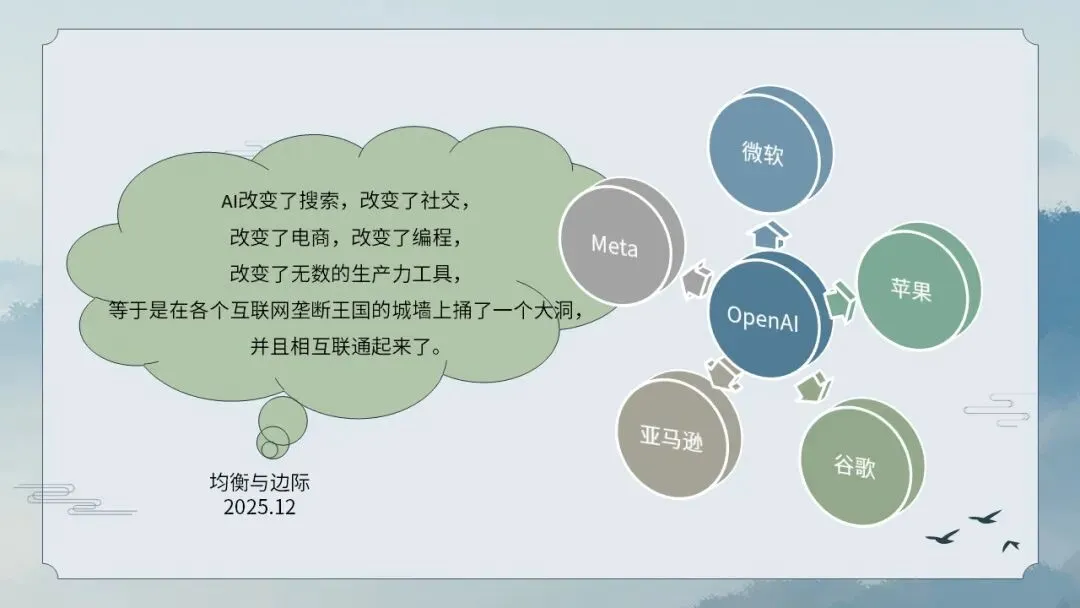

AI has upended search, social media, e-commerce, coding and countless productivity tools. In effect, it has breached the walls of every internet monopoly and connected them into a single contested terrain.

More than a decade ago, Microsoft, Apple, Google, Amazon and Meta—collectively FAAMG—forged highly mature business models, each ruling a corner of the internet as an autonomous fief with strong moat. Within these domains, they needed scant capital spending to sustain technological progress and rarely fought bitter battles, allowing them to earn effortless profits, known in investment jargon as **abundantly strong free cash flow**.

Since ChatGPT’s launch in late 2022, however, a strategic battlefield has opened at the heart of these monopolies. And prowling this arena is a disruptive force: OpenAI.

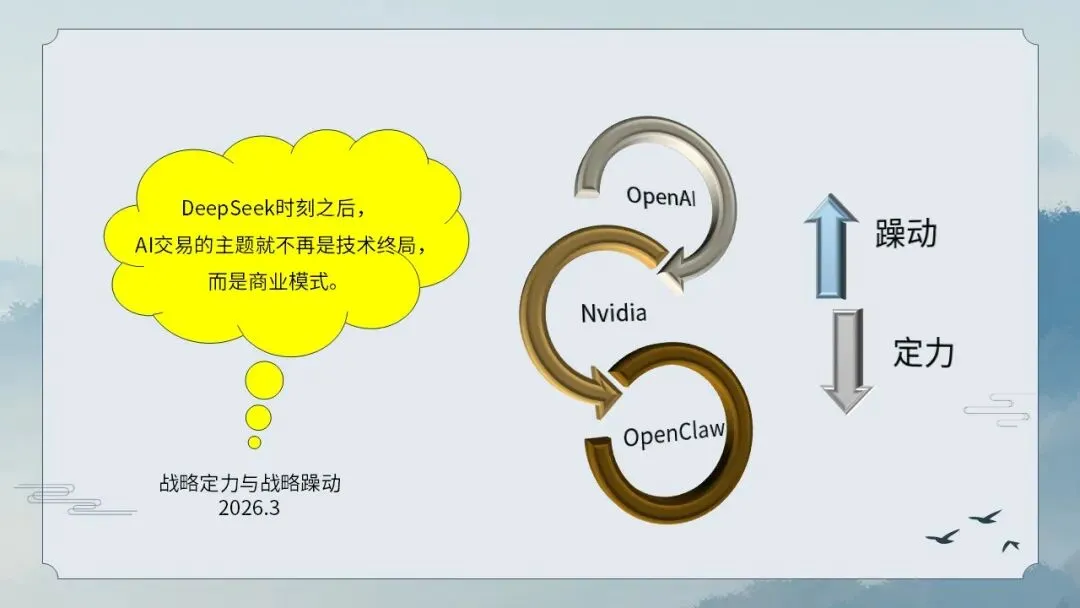

The DeepSeek moment in February 2025 offered America’s AI industry a chance to reset strategy. A collective decision to scale back capital expenditure and slow AI development could have yielded healthier finances and more sustainable technological progress.

Crucially, the other giants have escape routes: they can retreat to their fiefs and return to business as usual. OpenAI has no such sanctuary. So in mid‑2025, OpenAI joined forces with Nvidia and Oracle to announce moonshot‑scale capital spending plans. Once this arms race was ignited, every other giant fell into a **prisoner’s dilemma**. Fail to keep up, and a successful rival could devour your monopoly. All were thus dragged into an intensifying spiral of competition and capital escalation.

Such is the logic of being trapped on the tiger’s back. Hard data, drawn from corporate earnings, the US Federal Reserve and Bloomberg, underscores the trend.

Before ChatGPT’s late‑2022 debut, quarterly capital expenditure by the five FAAMG giants stood at roughly $20bn. It has since surged dramatically, now exceeding $120bn per quarter with no sign of easing. For context, quarterly US M2 growth ranges from $150bn to $200bn—putting the scale of AI investment into stark perspective.

Turning to quarterly free cash flow for the five groups: it rose steadily before 2023, peaking above $120bn. It has since collapsed, falling to just over $40bn. If this divergence persists, the five giants could turn **free cash flow negative** in 2026.

Should that happen, the repercussions will be profound. Fundamentally, FAAMG embodies America’s technological hegemony—the largest economic edifice built by the US since the Cold War and the dotcom era. They are also the backbone and anchor of America’s equity market. If even these giants exhaust free cash flow, the financial landscape will be transformed beyond recognition.

The impact on financial markets is more immediate. Share buybacks funded by free cash flow have been a cornerstone of America’s decade-long bull market. As outlined in previous speeches, dividends spread gains evenly, while buybacks selectively weed out less committed shareholders—a form of investor purification that powerfully props up share prices. A shortfall of hundreds of billions in annual buyback liquidity would spell severe consequences for US equities.

Win by resolve

The preceding analysis covers only the domestic dynamics of America’s artificial intelligence industry, excluding competitive pressures from China. Given today’s shifting landscape, I offer two decisive judgments. The first is:

**Since the DeepSeek moment, the defining theme of AI investment is no longer technological inevitability, but which business model will deliver it.**

AI is a fevered topic drawing comment from every corner. Capital markets, by contrast, tend to hold a more forward-looking understanding. Investors who attempt to price assets without updating on market consensus do so at their peril.

Some claim to be bullish on AI-related equities purely because they believe AI will transform the world. In voicing such optimism, they effectively declare the market underpriced—assuming their counterparts lack their insight into AI’s transformative potential, and that they can profit from this gap.

In reality, after the DeepSeek moment, AI’s world‑changing impact is no longer in doubt. Pricing is now driven primarily by business models. It is as if a debate rages over which university major offers the best career or postgraduate prospects, only for someone to interject that the child will grow up rather than perish young. The two are entirely irrelevant.

I advance a provocative thesis: **Beyond the DeepSeek moment, even if the United States were to disappear entirely, it would scarcely matter.** China and the rest of the world would still build the AI industry, still transform the globe, and still alter the course of history.

Stripping away national perspectives, this thesis can be restated: Even if all closed‑source models and their affiliated firms exited the market completely, open‑source communities and related enterprises would still advance the AI sector, reshape the world, and change history.

What is the difference? Without America and its closed‑source providers, the AI industry might advance more slowly and less efficiently. Yet its direction and end state would remain unchanged.

By way of analogy: AI is like Huangshan, a natural heritage that rightfully belongs to all humanity. Closed‑source model companies have installed cable cars and electric shuttles on the mountain. For convenience and efficiency, people may choose to pay. But such amenities are not indispensable. Through open‑source models, people can equally enjoy Huangshan’s beauty at low cost.

Leveraging the dominance of English‑language media, Wall Street seeks to perpetuate the illusion that **AI equals American closed‑source models, and American closed‑source models equal AI**. Dispelling this myth is a prerequisite for understanding the AI industry’s future. That is my first judgment, on the historical significance of the DeepSeek moment. My second is:

**The OpenClaw moment validates the technical and commercial vitality of open‑source models, squeezing closed‑source rivals on both operational performance and market confidence. **

America’s AI establishment understands DeepSeek’s significance perfectly well, yet it projects composure in public, dismissing open‑source progress as mere “distillation”. This tactic is familiar to China. At nearly every stage of its industrial ascent up the technology ladder, China has faced similar accusations—once labelled plagiarism or piracy, now distillation.

As long as open‑source models lag closed‑source alternatives in capability and efficiency, such accusations are hard to refute. As *The Analects* observes: “The gentleman abhors being in a lowly position; all the world’s evils are ascribed to him.” A catch‑up strategy carries the cost of bearing greater reputational pressure.

When does this dynamic end? When the follower outperforms the leader in at least one niche, delivering a genuinely original product or feature. For open‑source models, that inflection point has arrived: the OpenClaw moment.

OpenClaw enables unrestricted software calls—including those to other AI models—with full system permissions. This is a capability no closed‑source model has previously achieved. My focus, of course, is not on OpenClaw’s standalone potential; it remains immature and carries deployment risks. Yet this single step of originality redefines the meaning of the preceding 99 steps of catch‑up.

That is the technical dimension. Commercially, OpenClaw matters even more. Most closed‑source models use monthly subscriptions. Open‑source models have long offered token‑based metering, but mostly for business‑to‑business (B2B) use. The former resembles a gym membership; the latter, a utility bill. OpenClaw marks the first time utility‑style metering has been extended to mass consumer (C‑side) households.

The progression from DeepSeek to OpenClaw embodies one strategic logic. The US AI industry embodies another. The former relies mainly on back‑end, cost‑plus monetization. The latter leans on front‑end, brand‑premium pricing. The former’s competitive strategy rejects monopoly, pursuing survival in a hyper‑competitive landscape. The latter repeats the internet playbook: “burn capital first, monopolize later”.

When these two strategic logics collide, the former is prepared for prolonged relative weakness, steadily eroding casual users with low costs, shrinking the latter’s comfortable territory, containing unrest with steady strategy, waiting for a decisive strike—or simply letting rivals self‑destruct under pressure.

For American closed‑source models, victory has only one form: generating trillions of dollars in end‑user revenue within years. Failing that, they will be consumed by depreciation and operating costs. Any outcome short of this amount to a win for open‑source models.

Grasping this structure clarifies their interdependent and adversarial relationship. The more resolve the former, the more restless the latter becomes. The more agitated the latter, the more the former must hold its nerve.

One final point: Even absent open‑source competition, America’s AI industry’s competitive strategy is likely flawed.

Sociology and psychology identify a concept known as the “winner’s curse”. A classic example is the US military. The lopsided success of the 1991 Gulf War led to equipment—from Humvees to arsenal ships—designed for asymmetric, one‑sided combat. When facing peer‑level systemic competition, it quickly became overstretched.

In my view, America’s AI industry’s replication of the internet’s “burn capital, then monopolize” playbook has also fallen victim to the winner’s curse. First‑mover advantage, mindshare, network effects, user stickiness, lower customer acquisition costs—all rest on products having network effects. Simply put: if the first 99 users choose a product, the 100th has little choice but to follow. That defined the internet era.

Most AI products, however, lack network effects. What others use is irrelevant to me. Most users already employ multiple overlapping AI tools, even actively cross‑checking the same query to guard against hallucinations. For AI products, racing to launch and capturing mindshare carries little weight.

Today, Gemini and Claude are gaining ground rapidly, and ChatGPT’s brand loyalty offers little protection. OpenAI’s responses include partnering with Department Of War on lethal technologies, inserting advertisements into AI responses, and partially relaxing adult‑content restrictions—classic restlessness born of crisis.

Naturally, the mantis stalks the cicada, unaware of the oriole behind. The troubles besetting OpenAI today will confront Google and Anthropic tomorrow. Such is the AI industry’s divergence from the internet.

The Greater Fool

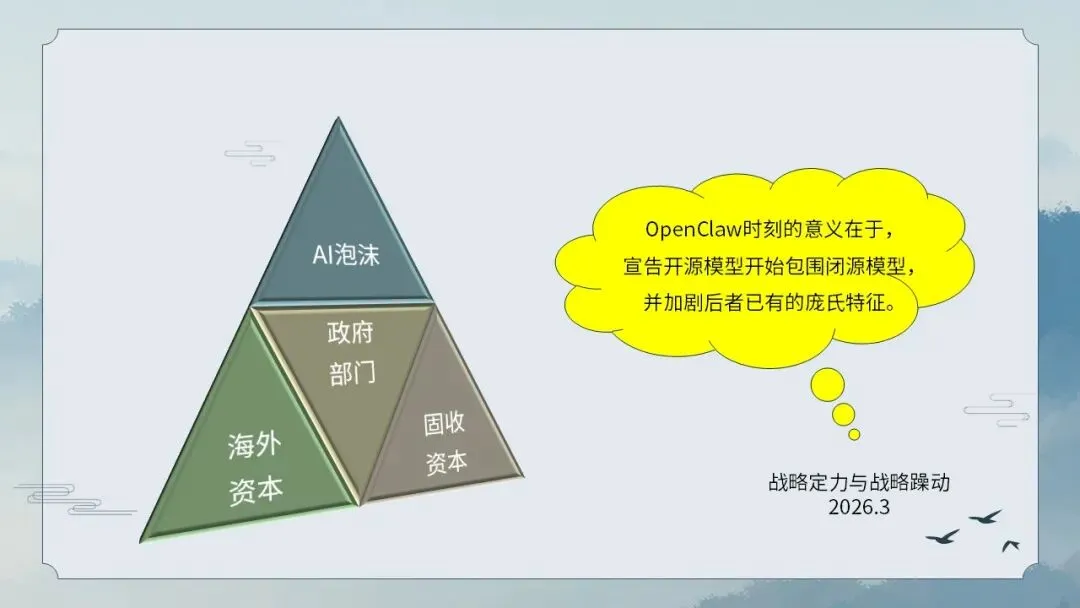

Amid intensifying internal strains and external competition, the strategic restlessness of America’s AI industry threatens to turn into an ever more reckless financial spectacle, pushing capital expenditure and asset prices to unsustainable extremes. The nagging question remains: where will the money come from? The single biggest dilemma plaguing America’s AI sector today is its desperate search for **the greater fool**.

America’s IPO market is set for a bumper year in 2026. Three giants—SpaceX, OpenAI and Anthropic—have all announced plans to list within the year, carrying a combined valuation of more than $3trn.

History shows that mega‑IPOs often signal a bull market peak. The logic is simple: for secondary‑market investors, a flotation is a chance to buy; for controlling owners, it is a chance to sell. Sellers hold the upper hand.

In the past, firms went public partly out of necessity to raise capital. Today, America’s deep private equity and private credit markets can meet almost any funding need. The public markets are only tapped when private pools have been fully drained.

I do not predict with certainty that American equities will peak in 2026. But logically, the risk‑reward balance of the US AI industry has already deteriorated sharply. To sustain an even grander narrative, still bigger greater fools will be needed.

US stock valuations have become deeply distorted. America accounts for roughly 25% of global GDP but boasts more than 60% of global equity market capitalization. The top five firms make up over 30% of that total. NVIDIA alone is worth nearly half the CSI 300 index. Without massive foreign capital inflows, extending the long bull run looks implausible.

Who might these greater fools be? Three groups stand out: overseas capital, fixed‑income investors and the state.

Foreign appetite for American assets has possibly peaked and is fading. The dollar’s purchasing power is eroding, yet its exchange rate remains strong. In technical terms, the capital account has overtaken the current account as the market’s main driver. Put plainly: investors hold dollars not to buy goods, but to trade stocks.

Consumption is steady; financial speculation is not. Those who unite for profit will disperse when profits dry up. In this light, 2025 marks a pivotal turning point. The ratio of MSCI World ETF to S&P 500 ETF shows that American assets have outperformed non‑American ones for more than a decade—yet this super‑trend finally reversed in 2025. Its significance is profound.

An asset that has risen uninterrupted for over ten years is likely to face a deep, prolonged correction once the tide turns. After a decade‑long rally, all bears have been squeezed out, leaving a lopsided pricing structure that theoretically favors gains over losses—much like prime property in China’s first‑tier cities before recent years. A reversal, then, may signal far deeper shifts at work.

Beyond foreign capital, America hosts a vast pool of fixed‑income capital keen to allocate to big tech. Fixed‑income portfolios need sectoral balance; they cannot overload on capital‑intensive industries simply to meet funding demand. Large tech firms generate stable free cash flow, making them appealing credit targets. Yet a paradox arises: precisely because their cash flow is reliable, they traditionally need little borrowing. Google and Meta once carried no debt at all.

That has changed dramatically since 2025. Nearly every big tech group has been issuing debt aggressively. Google even plans to sell 100‑year euro‑denominated bonds. For all Google’s strength, the firm is just 28 years old—a 100‑year maturity stretches credibility. Amazon, Meta, Apple and Microsoft have also sold 40‑ and 50‑year debt, longer than the 30‑year maximum for US Treasuries.

More importantly, this borrowing wave is on an epic scale, often running to hundreds of billions of dollars. For fixed‑income investors, the bonanza has arrived too suddenly. It feels like a long‑cherished ideal suddenly proposing marriage—one cannot help but wonder why.

Oracle offers a cautionary tale. Long a favorite of bond investors, the veteran tech firm entered circular financing arrangements with OpenAI and NVIDIA in 2025. Its 20‑year record of steady free cash flow turned negative; its 10‑year credit default swap spread briefly neared 250 basis points, pushing it into junk territory; and its share price fell below pre‑partnership levels.

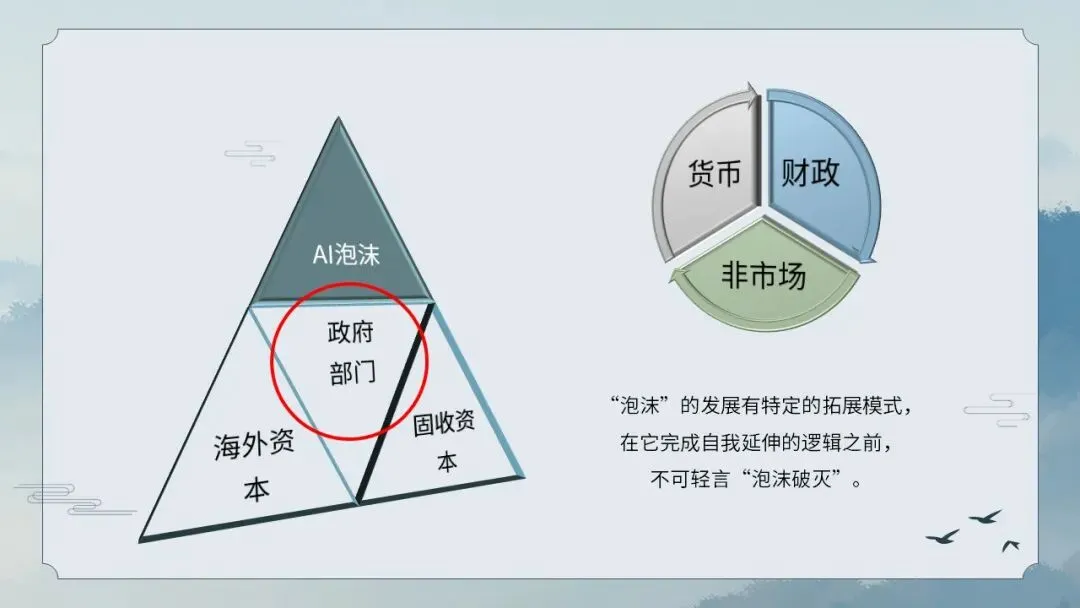

The ultimate greater fool for America’s stock market may well be the US government—both monetary and fiscal. Though last in line, it will be the most powerful backstop. Should markets crash and economic crisis loom, expect no monetary or fiscal discipline. Policymakers will cast aside all constraints to intervene: cutting interest rates to zero, restarting quantitative easing, fiscal handouts, halting antitrust probes, direct market intervention, pressing foreign governments for favors, and even stoking geopolitical unrest to drive capital home.

As argued in *Comparative Studies of Two Global Crises*: A bubble follows its own logic of expansion; it cannot be dismissed as burst until that logic has run its course.

Yet prices will eventually revert to fundamentals. Should America’s AI business model prove unworkable, a short opportunity akin to 2008 will re‑emerge.

Human nature is unchanging; history repeats itself. There is nothing new under the sun.

The HALO Trade

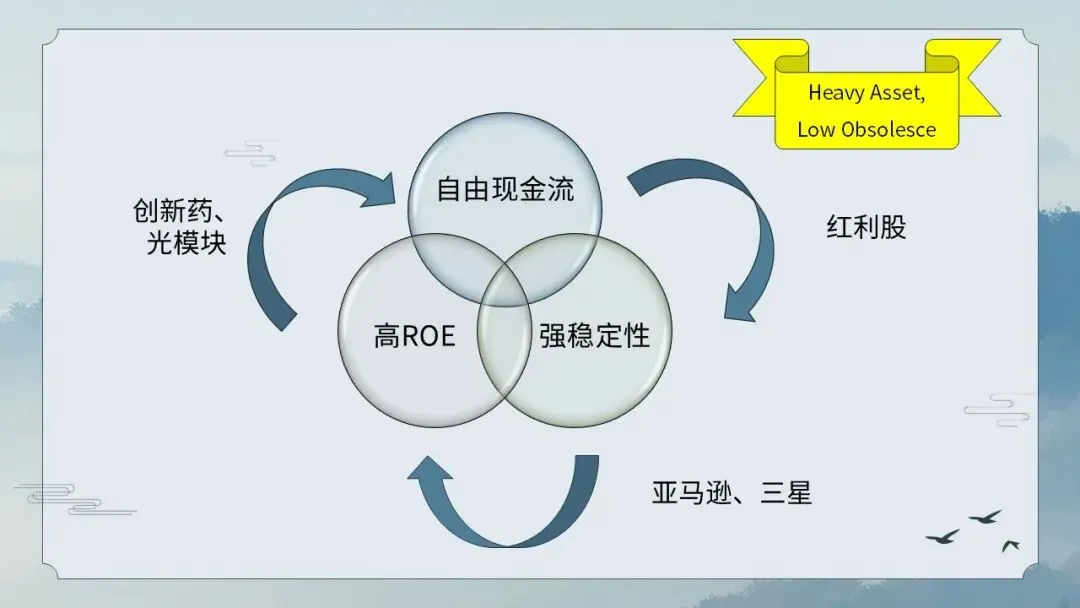

Turning back to equity markets, the HALO trade has surged in popularity since 2026. HALO stands for **Heavy Asset, Low Obsolescence**. In truth, the HALO trade is simply dividend investing.

I here propose an impossible trinity: a listed company cannot simultaneously combine **free cash flow, high ROE and strong stability**. This holds true in general, with rare exceptions.

Firms with free cash flow and high ROE—such as innovative drugmakers and optical module producers—cannot be stable. Exceptional profits invite rivalry; all of Porter’s five forces turn hostile.

Can firms combine high ROE and stability? Possibly—but only by giving up free cash flow. Amazon, Samsung and TSMC fit this model. They plough every cycle’s profits back into the next. By never resting on gains, they stay ahead.

The third path: abandon high ROE to pursue stability and free cash flow. That defines classic dividend stocks. A business with steady operations and ample free cash flow will naturally pile up excess cash; not paying dividends becomes odd.

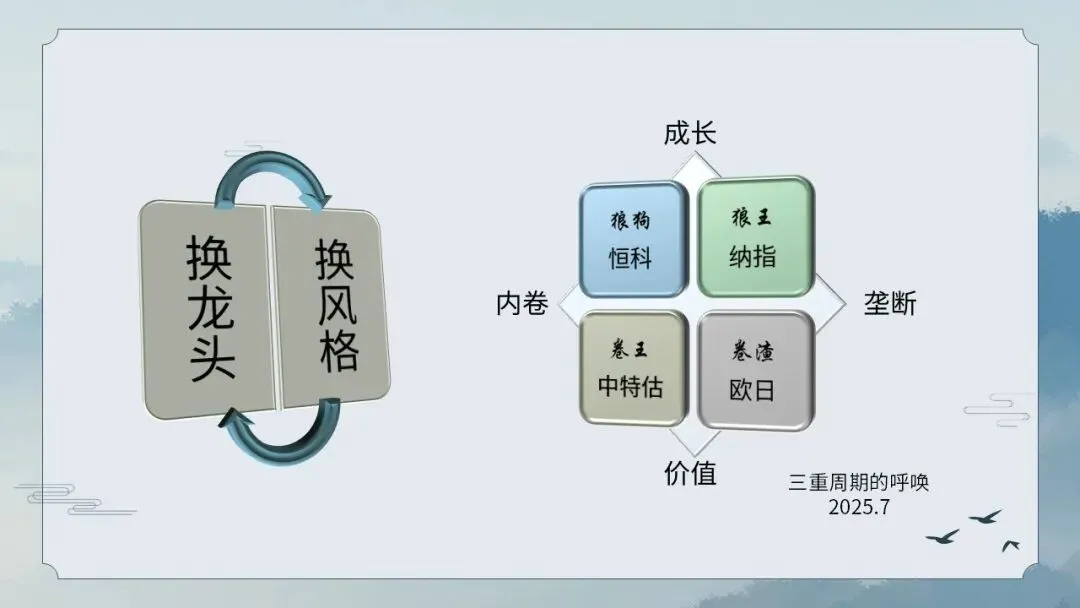

The HALO trade, then, is fundamentally a dividend strategy. From a global allocation perspective, I add a key rule: **a shift in market leaders demands a shift in style, and a shift in style demands a shift in leaders**.

I first laid out this idea in my July 2025 speech *The Call of Three Cycles*. I divide markets into **involuted (hyper‑competitive)** and **monopolistic**, and stocks into **growth** and **value**:

- Monopolistic markets + growth stocks = the Alpha Wolf, exemplified by the NASDAQ

- Involuted markets + growth stocks = the Wolfhound, exemplified by the Hang Seng Tech Index

- Monopolistic markets + value stocks = the Stagnant Incumbent, exemplified by European and Japanese firms

- Involuted markets + value stocks = the Resilient Value King, exemplified by China’s state‑owned enterprise valuation theme

Some investors believe in an East‑rises‑West‑declines narrative yet shun China’s state‑owned enterprise theme. They rotate from Alpha Wolves to Wolfhounds—changing leaders without changing style. While short‑term results are unclear, strategically this logic lacks long‑term merit.

The HALO trade suffers a similar flaw. Wall Street now sees AI bubble risks but only diversifies into Europe, Japan and the Russell 2000. This is shifting style without shifting leaders—and in my view, equally misguided.

The above analysis is for discussion only and does not constitute investment advice.