文档内容

Guidelines

Welcome to the first step of the recruitment process at Bain & Company, Inc. You are about to get a firsthand

experience on practical Bain casework. The test is based on modified Bain cases and is designed to assess your

approach to problem solving using strategic thinking and deductive reasoning. At Bain, we are more interested in

‘how you think’ rather than ‘what you’ve learnt’.We work on diverse complex situations spanning across multiple

industries and sectors, but present only concise, relevant information to our clients. In order to do the same, we

understand the data, interpret the insights, and finally present what we infer in an organized manner. This test is

designed to simulate the same experience for you!

While attempting this paper:

! Understand:Read the case studies carefully and identify the underlying problem. Make sure you do not

leave out any inputs or key data points

! Interpret:Focuson detailsin the text and charts. Pay attention to the period of analyses and units used

! Structure your approach: Manage your time by answering the questions smartly. For instance, some

questions do not require calculations but only involve simple elimination of choices. Always do a quick check

before answering

Instructions

! This booklet consists of 25questionswith multiple choices. Each question has a single correct answer

! It not necessary to answer allquestions. You mayattempt these questionsaccording toyour strengths and

time.Read the question extremely well and attempt it only when you have fully understood what is to be

done

! Use of any electronic devices (calculators, mobile phones, etc.) is strictly prohibited while answering the

test

You have 60 minutes to complete the test. Keep your composure and best of luck!CASE STUDY 1

Grocery Co is a global retailer existing inChinafor more than a decade now. With the appointment of a new CEO

and rehaul of the top management team, China is a global growth priority for the company.

China’s grocery retail market has strong regional characteristics with consumer tastes differing across regions and

with local brands in demand. There is large income gap and average household income is low compared to other

developed markets. There is emphasis on fresh foods and leading players are investingmore in it to draw traffic.

The distribution network is fragmented with cold chain almost non-existing.

Grocery Co is under-performing in almost all dimensions thatmatter, especially in comparison tothe market

leader. Sales productivity (per store and per sq. meter) and profitability are low and the organization is skeptical of

change due to previously failed attempts. As communicated by the management, stretched goals and expansion

plans, resulting in ineffective decision-makingand undesirable behaviors,led to the failure of past attempts to

bring a change in the organization.

New senior management team is not aligned yet, both internally and as well as with global stakeholders. New CEO

engaged Bain to help him assist in buildinga100 daysplanto address the issues by conducting an objective

assessment of the business and industryto guide consistent andtough decisions.

Q1. Which of the following most accurately describes why Grocery Co. hasapproached Bain?

a. To analyze the Chinese grocery market andlook for possible acquisitions

b. To understand the scope for further development of sales

c. To help the new CEO understand the business and get up to speed

d. To build a transformation roadmap and support teams on key initiatives implementation

Q2. Which of the following information will be least useful for Bain in addressing the client’s needs?

a. Benchmarking metrics and data on its competitors’ profitability

b. Market overview

c. Decision effectiveness data

d. Organization structure

Q3. Bain approached the case with three sequential modules:

A. Focus on formulation of strategy and high-level organization design

B. Focus on detailed strategy translationand execution across entire organization

C. Assess broad set of issues for Grocery Co. and focus on big issues with some detailed analysis

From the above information what was the course of action according to you?a. A→C→B

ob. C→A→B

c. B→C→A

d. C→B→A

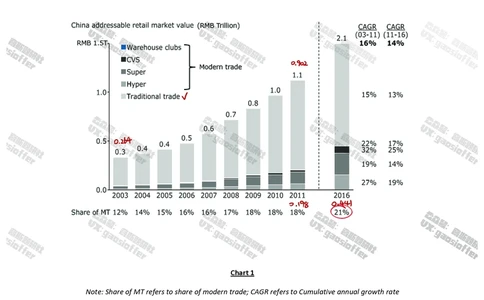

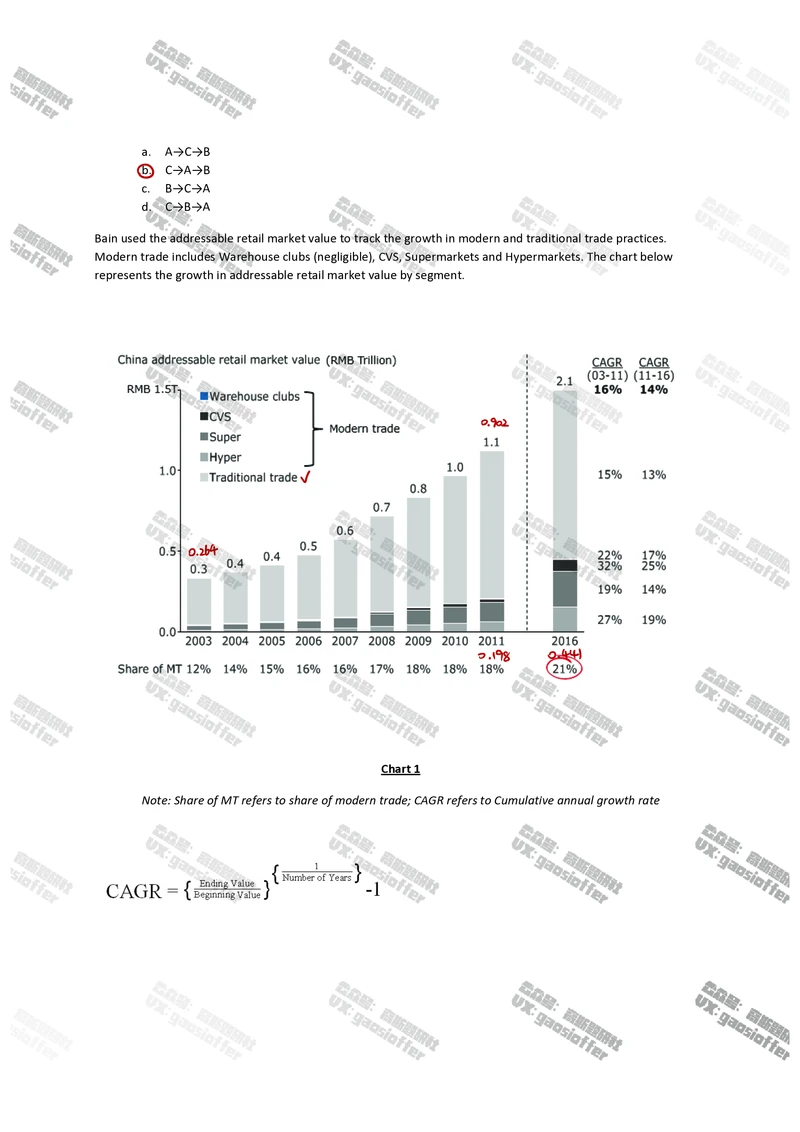

Bain used the addressable retail market value to track the growth in modern and traditional trade practices.

Modern trade includes Warehouse clubs (negligible), CVS, Supermarkets and Hypermarkets. The chart below

represents the growth in addressable retail market value by segment.

o902

0

0.264

0.198 0.441

Chart 1

Note: Share of MT refers to share of modern trade;CAGR refers to Cumulative annual growth rateQ4. The addressable retail market value is a combination of modern and traditional trade practices. What is the

overall increase in the addressable retail market value for traditional trade in China between 2003 and 2011?

a. 80-110%

b. 130-160%

c. 180-200% iii! 240

d. 230-250%

Q5. What is the cumulative annual growth rate(CAGR)for 2011-16 for modern trade?

a. ~28%

b. ~25%

c. ~17%

d. ~14% (cid:16175) F 1

14.27

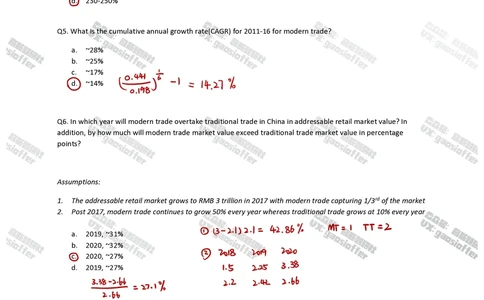

Q6. In which year will modern trade overtake traditional trade in China in addressable retail market value? In

addition, by how much will modern trademarket value exceed traditional trade market value in percentage

points?

Assumptions:

1. The addressable retail market grows to RMB 3 trillion in 2017 with modern trade capturing 1/3rdof the market

2. Post 2017, modern trade continues to grow 50% every year whereas traditional trade grows at 10% every year

a. 2019, ~31% D 3 21 2.1 42.86 ME1 TT 2

b. 2020, ~32%

0c. 2020, ~27% 618 2019 2020

d. 2019, ~27% 1.5 225 3.38

3 (cid:8489)(cid:2191)

27.1

22 242 2.66

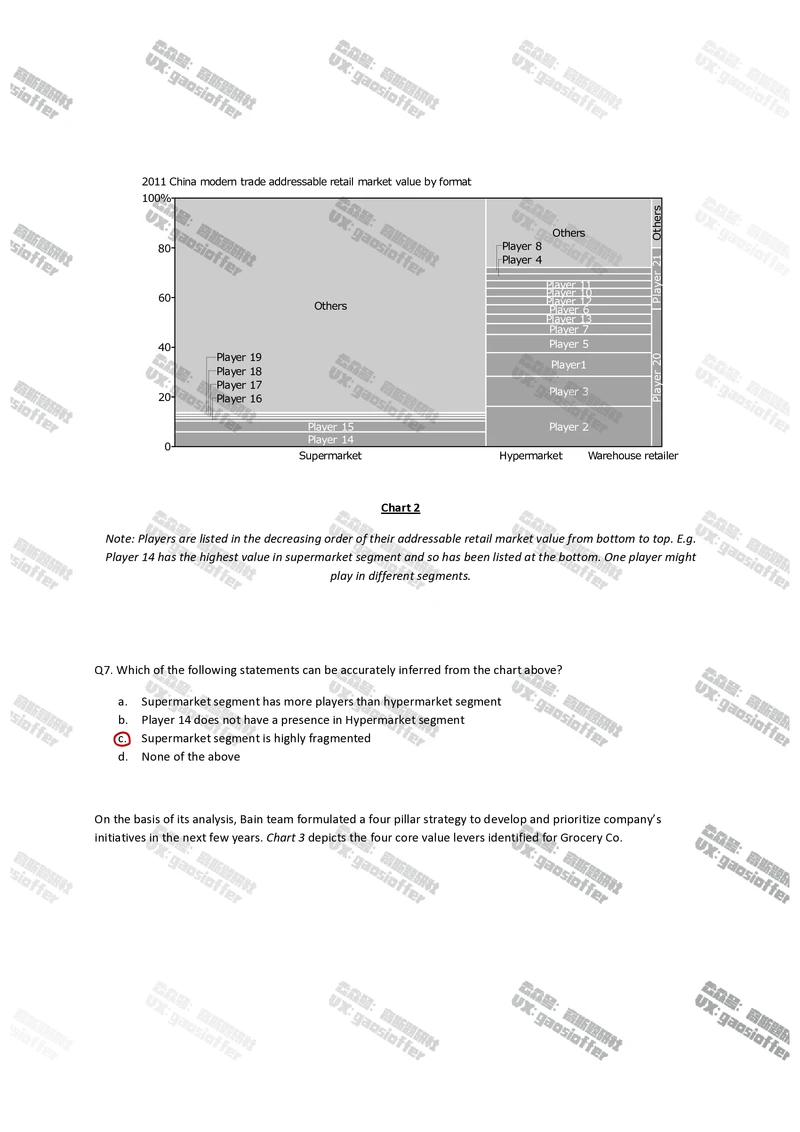

The company’s CEO wants Bain to chart the competitor landscape in the grocery market (modern trade) to get a

better picture and devise appropriate strategies to capture a more share in the market.100%

Others

80

Player11

Player10

60 Player12

Others Player6

Player13

Player7

40 Player5

Player1

Player3

20

Player15 Player2

Player14

0

Supermarket

srehtO

12reyalP

02reyalP

2011Chinamoderntradeaddressableretailmarketvaluebyformat

Player8

Player4

Player19

Player18

Player17

Player16

Hypermarket Warehouseretailer

Chart 2

Note: Players are listed in the decreasing order of their addressable retail market value from bottom to top. E.g.

Player 14 has the highest value in supermarket segment and so hasbeen listed at the bottom. One player might

play in different segments.

Q7. Which of the following statements can be accurately inferred from the chart above?

a. Supermarket segment has more playersthan hypermarket segment

b. Player 14 does not have a presence in Hypermarket segment

c. Supermarket segment is highly fragmented

d. None of the above

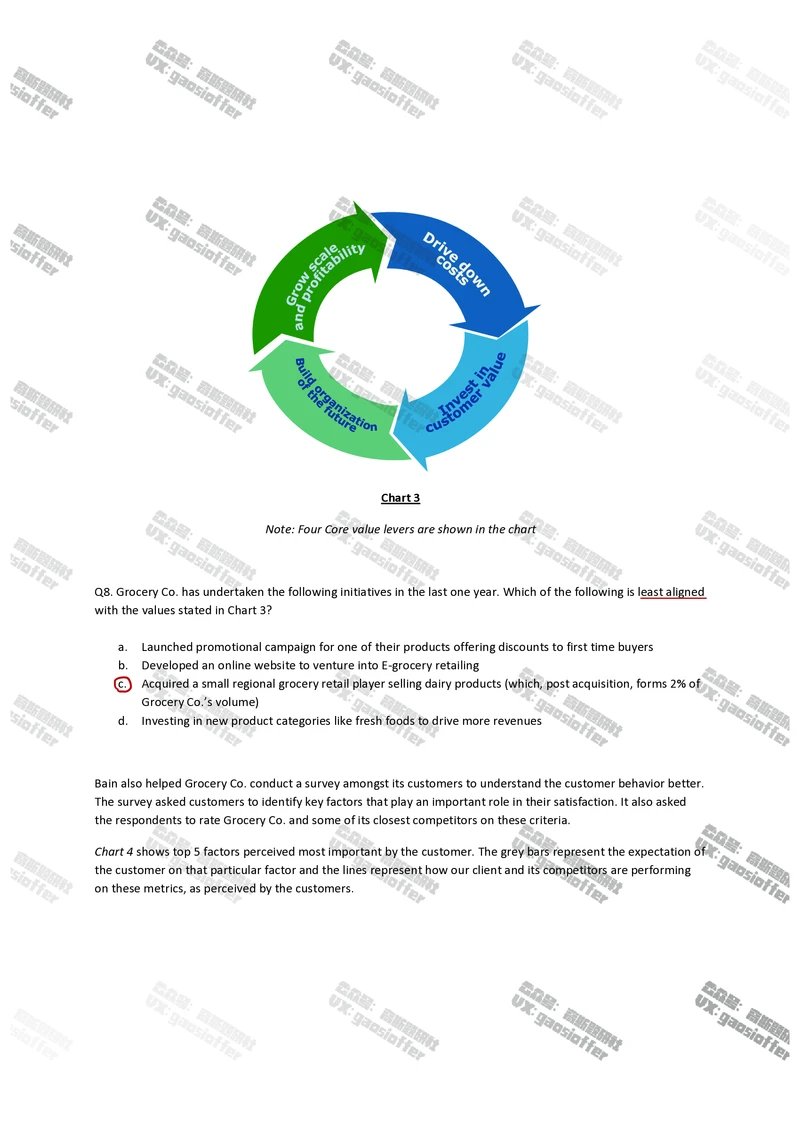

On the basis of its analysis, Bain team formulated a four pillar strategy to develop and prioritize company’s

initiatives in the next few years. Chart 3depicts the four core value levers identified for Grocery Co.Chart 3

Note: Four Core value levers are shown in the chart

Q8. Grocery Co. has undertaken the following initiatives in the last one year. Which of the following is least aligned

with the values stated in Chart 3?

a. Launched promotional campaign for one of their products offering discounts to first time buyers

b. Developed an online website to venture into E-grocery retailing

oc. Acquired a small regional grocery retail player selling dairy products (which, post acquisition, forms 2% of

Grocery Co.’s volume)

d. Investing in new product categories like fresh foods to drive more revenues

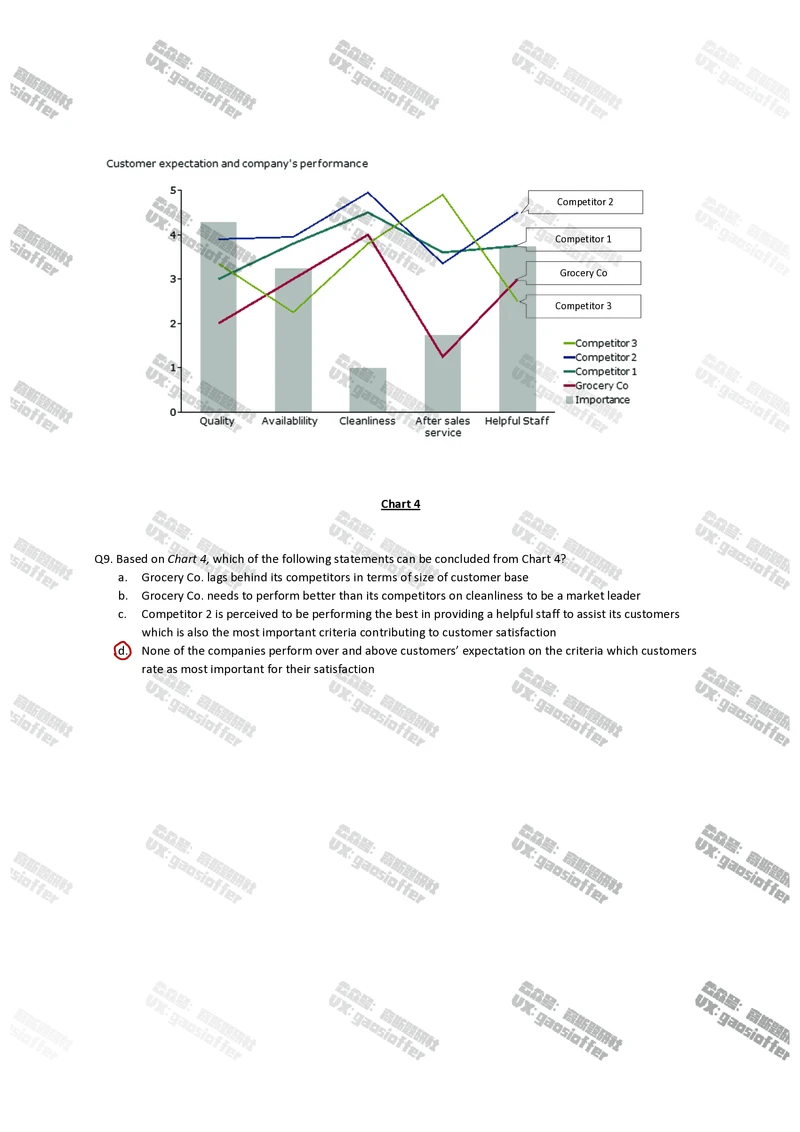

Bain alsohelped Grocery Co. conduct a survey amongst its customers to understand the customer behavior better.

The survey asked customers to identify key factors that play an important role in their satisfaction. It also asked

the respondents to rate Grocery Co. and some of its closest competitors on these criteria.

Chart 4shows top 5 factors perceived most important by the customer. The grey bars represent the expectation of

the customer on that particular factor and the lines represent how our client and its competitors are performing

on these metrics, as perceived by the customers.Competitor 2

Competitor 1

Grocery Co

Competitor 3

Chart 4

Q9. Based on Chart 4,which of the following statements canbe concluded from Chart 4?

a. Grocery Co. lags behind its competitors in terms of size of customer base

b. Grocery Co. needs to perform better than its competitors on cleanliness to be a market leader

c. Competitor 2 is perceived to be performing the best in providing a helpful staff to assist its customers

which is also the most important criteria contributing to customer satisfaction

od. None of the companies perform over and above customers’ expectation on the criteria which customers

rate as most important for their satisfactionCASE STUDY 2

Our client, Toy Co is a leading MNC with toys as its core business and operates licensing model in other consumer

products categories. Toy Co has identified licensing business as a key growth driver. Of its brand portfolio, 2 brands

have been identified as thefocus of the project; one of them has been operating licensing business in China across

~40 product categories and the other has presence in 1 category only.

China licensing market is currently small, both in absolute and relative terms. This is attributed to issues of high

fees paid as royalty, and generally lower consumer savings driven by high taxes, respectively. Compared to

developed countries, the consumer spend on such products is also low. Licensing market is fragmented with over

800 licensors; Disney, the leading player, accounts for only ~10% market share. There are ~9 macro categories in

the China licensing market of which Apparel, Entertainment/Service, Home and Footwear are expected to lead the

growth in the coming years.

Licensing market in China is supply-based as majority of consumers cannot differentiate licensed from self-

operated products. China’s consumer spend on overall consumer products expects double digit annual growth; led

by Food, Electronics and Apparel sectors.

Licensing can be done through multiple ways. The most prevalent are Brand (Lego, BMW), Character (Mickey

Mouse, Superman) and others like NBA and Harvard University. Loosening of restrictions on comic movies and

popular marketing events have increased character awareness; brand is relatively established compared to

character.

The CEO of Toy Co, an old friend of the Bain Partner, believes that licensing opportunities in mainland China were

not fully understood nor captured. Despite having been in the licensing business in China for quite some time, the

revenue is still insignificant. Also, there is a lack of collaboration between the core toy and licensing businesses to

take advantage of synergies (in terms of marketing & channels).

(cid:1246)

Q10. Which of the following most accurately describes why the client engaged Bain & Company?

a. The client wishes to analyze why his revenue growth is slow in the Chinese market

b. The client seeks to know if the Chinese toy market is already saturated

c. The client wants Bain to develop and strategize their China licensing plan

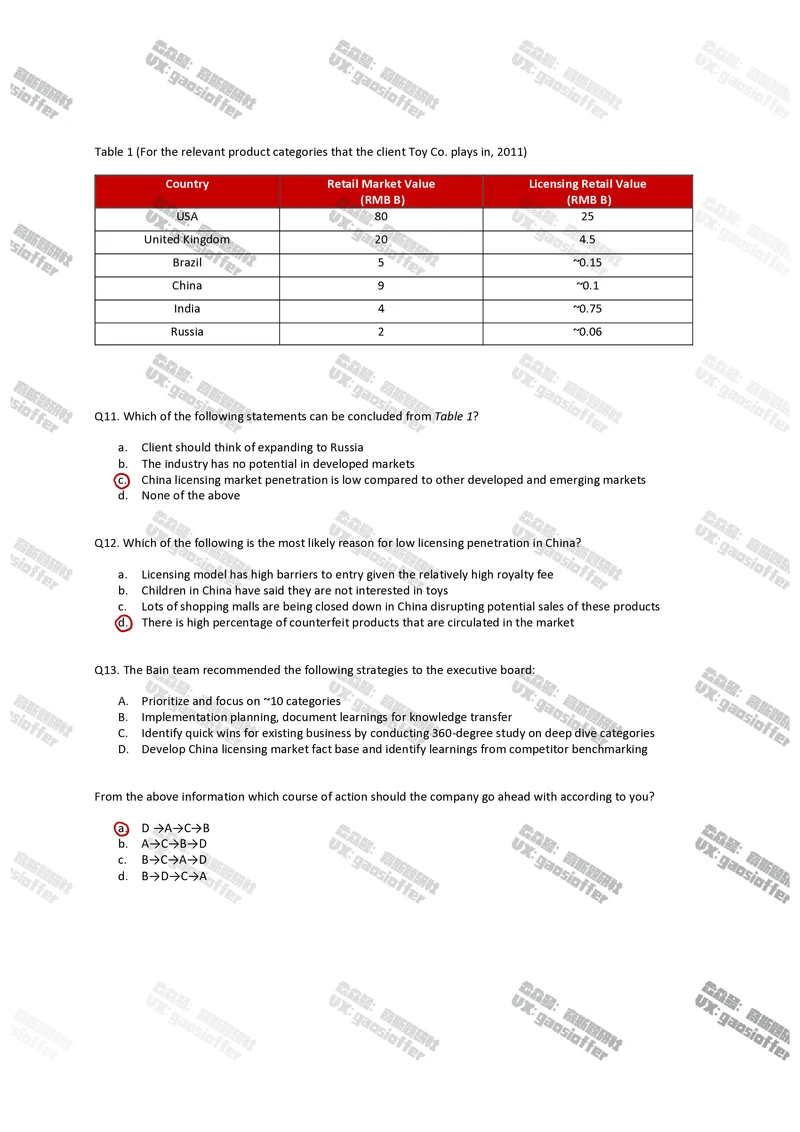

d. The client wants to Bain to devise an exit strategyTable 1 (For the relevant product categories that the client Toy Co. plays in, 2011)

Country Retail Market Value Licensing Retail Value

(RMB B) (RMB B)

USA 80 25

United Kingdom 20 4.5

Brazil 5 ~0.15

China 9 ~0.1

India 4 ~0.75

Russia 2 ~0.06

Q11. Which of the following statements can be concluded from Table 1?

a. Client should think of expanding to Russia

b. The industry has no potential in developed markets

oc. China licensing market penetration is low compared to other developed and emerging markets

d. None of the above

Q12. Which of the following is the most likely reason for low licensing penetration in China?

a. Licensing model has high barriers to entry given the relatively high royalty fee

b. Children in China have said they are not interested in toys

c. Lots of shopping malls are being closed down in China disrupting potential sales of these products

od. There is high percentage of counterfeit products that are circulated in the market

Q13. The Bain team recommended the following strategies to the executive board:

A. Prioritize and focus on ~10 categories

B. Implementation planning, document learnings for knowledge transfer

C. Identify quick wins for existing business by conducting 360-degree study on deep dive categories

D. Develop China licensing market fact base and identify learnings from competitor benchmarking

From the above information which course of action should the company go ahead with according to you?

oa. D →A→C→B

b. A→C→B→D

c. B→C→A→D

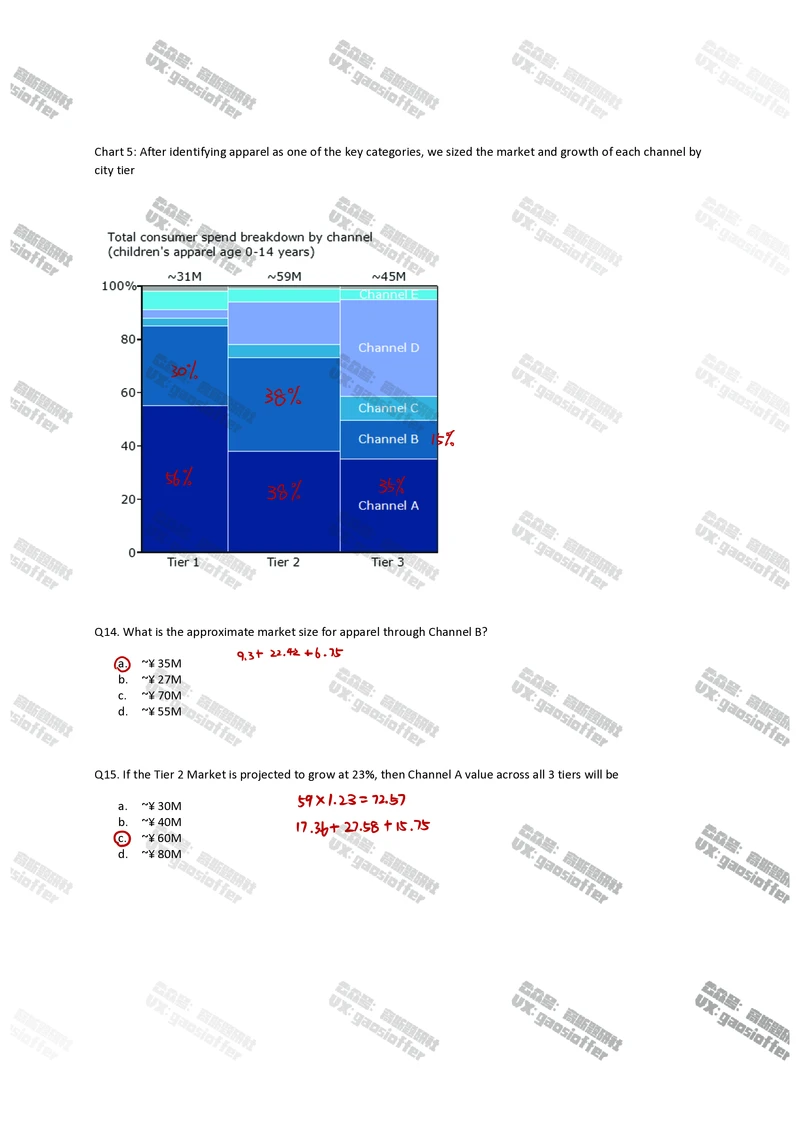

d. B→D→C→AChart 5: After identifying apparel as one of the key categories, we sized the market and growth of each channel by

city tier

30

38

15

56

35

38

Q14. What is the approximate market size for apparel through Channel B?

9.3 22.4216.75

oa. ~¥ 35M

b. ~¥ 27M

c. ~¥ 70M

d. ~¥ 55M

Q15. If the Tier 2 Market is projected to grow at 23%, then Channel A value across all 3 tiers will be

a. ~¥ 30M 59(cid:1066)1.23 72.57

b. ~¥ 40M

17.36 27.58115.75

c. ~¥ 60M

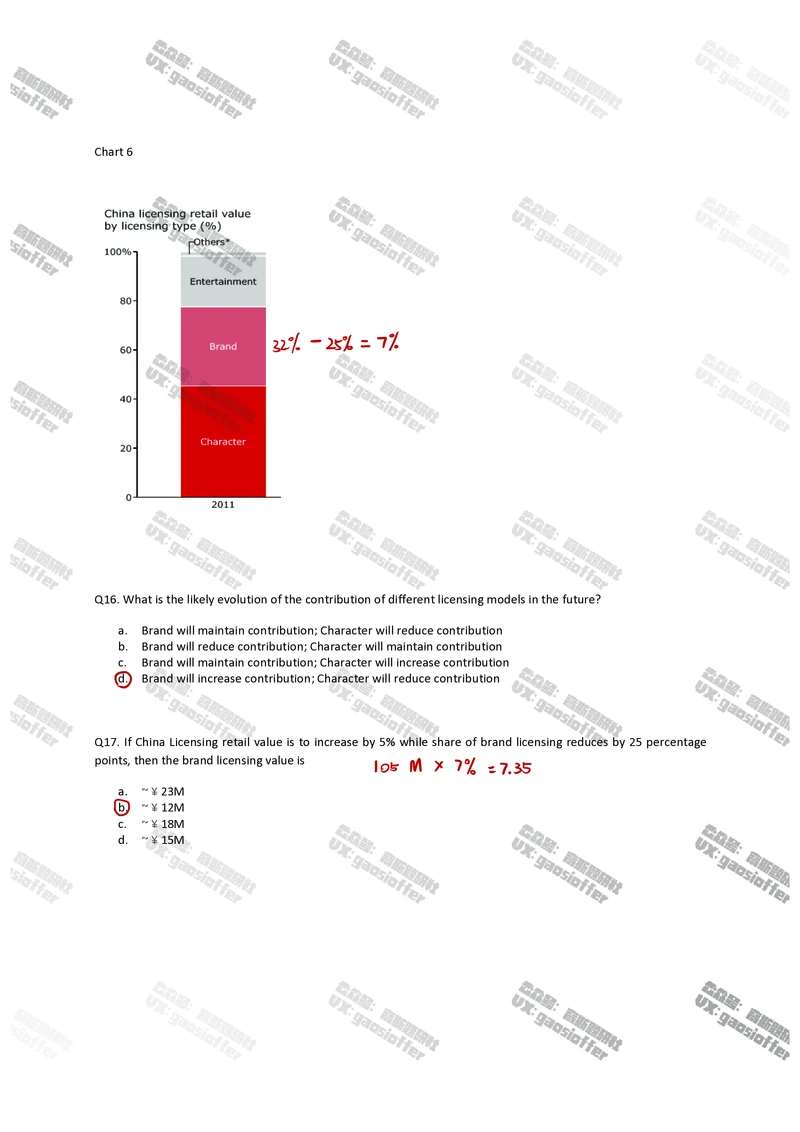

d. ~¥ 80MChart 6

32 25 7

Q16. What is the likely evolution of the contribution of different licensing models in the future?

a. Brand will maintain contribution; Character will reduce contribution

b. Brand will reduce contribution; Character will maintain contribution

c. Brand will maintain contribution; Character will increase contribution

d. Brand will increase contribution; Character will reduce contribution

Q17. If China Licensing retail value is to increase by 5% while share of brand licensing reduces by 25 percentage

points, then the brand licensing value is

105M X 7 7.35

a. ~ ¥ 23M

b. ~ ¥ 12M

c. ~ ¥ 18M

d. ~ ¥ 15MCASE STUDY 3

Pharma Co.is one of China’slargest pharmaceutical companies. Headquartered in Beijing, the companyhas a wide

range of successful products on the markets that include various drugs for erectile dysfunction, lowering blood

cholesterol, anxiety disorders, anti-inflammatory drugs, antidepressants, etc.

Currently, the client has only one product in the market for cancer treatment (FC-600) which generated RMB200M

sales in 2014. In the next 1 year, the client is planning to introduce a new cancer drug in the market. This particular

drug, RFC-9000, will also be for cancer patients and if taken in combination with FC-600, it will speed up treatment

process. There is no other drug available in the market similar to RFC-9000 and the drug will be first of its kind. The

current sales force includes 750 sales representatives who support the company's cancer drug that is already in the

market. The management is still in the planning phase and has taken no concrete steps for introduction of the drug

in the market. The CEO of Pharma Co., Mr.Yang, also wants to file for approval from CFDA (China Food and Drug

Administration), which he feels would not take much time and money.

Pharma Co. has two alternatives available with it to go forward with the manufacture of RFC-9000. First alternative

isto produce it in-house. In-house production will involve incurring of significant production costs, as production of

this drug requires use of advanced technology. An alternative route is to outsource the production of the drug to

other companies. Under the outsourcing agreement, Pharma Co. will utilize the production facilities and

technology of the outsourcer, but will provide its own raw material and ingredients for the drug. However, there

can be stringent terms and conditions imposed by each of these companies on Pharma Co. which Mr. Yang is still

to look at.

Upon discussion with Mr. Yang, Bain has found out that divergent views exist on the two alternatives available

among the top management, which is resulting in delay of production and launch.

Mr. Yangwants Bain to investigate the issue in detail and devise a blueprint for the future. Bain has a team of five

members on the case and you are the Associate Consultant on the team. In your opinion:

Q18. Which of the following most accurately describes why Pharma Co.approached Bain?

a. To resolve the differences of opinion on alternatives of production routes among top management

b. To understand the scope customer audience for RFC-9000

c. To devise a comprehensive production and launch strategy for Pharma Co.

d. To decide which production route should Pharma Co. opt for

Q19. What are the sequence of steps that Pharma Co. should follow before going forward with the launch of the

product?

1. Seek approval from CFDA to go ahead with launch of RFC-9000

2. Deviselaunch strategy and put in place a trained and knowledgeable marketing team in place

3. Analyze cost implications of the various production alternatives available and their impact on profitability

4. Quantify challenges and assess current market share of other companies producing the cancer drugs

a. 1432b. 1342

c. 3241

d. 2143

Q20.Which of the following is not a potential cost for Pharma Co. irrespective of producing RFC-9000 in-house or

outsourcing production?

a. Marketing costs

ob. Sales and distribution costs

c. Research and development costs

d. Costs of ingredients/ raw material

Pharma Co. claims that if RC-9000, the new drug, is taken in combination with FC-600 (already existing drug), the

recovery process of cancer patients will pace up. Hence, Mr. Yang believes that Pharma Co. has a ready customer

audience for the new drug.

According to statisticsreported in 2015, the population of China is 1.5B out of which 1% of the population suffers

with cancer. It is expected that population of cancer patients will increase by 2% every year in future.

As reported by Pharma Co., FC-600 is consumed by 2/3rd of the current cancer patient population in China (as of

2015). This is expected to remain constant in the forthcoming years. Also, it is projected that the acceptance by

current consumers for RFC-9000 will be 60% in the first year of launch and will increase by 10 percentage points

every year.

Q21. The company goes forward with the launch of RFC-9000 in 2016. What will be the total number of cancer

patients consuming RFC-9000 by the end of first year?

(cid:2974)5

zob

a. 10,200,000

D nooooooo 5(cid:1319)oooox !

b. 9,120,000

c. 6,200,000 nooooox

go

d. 6,120,000

612ooo

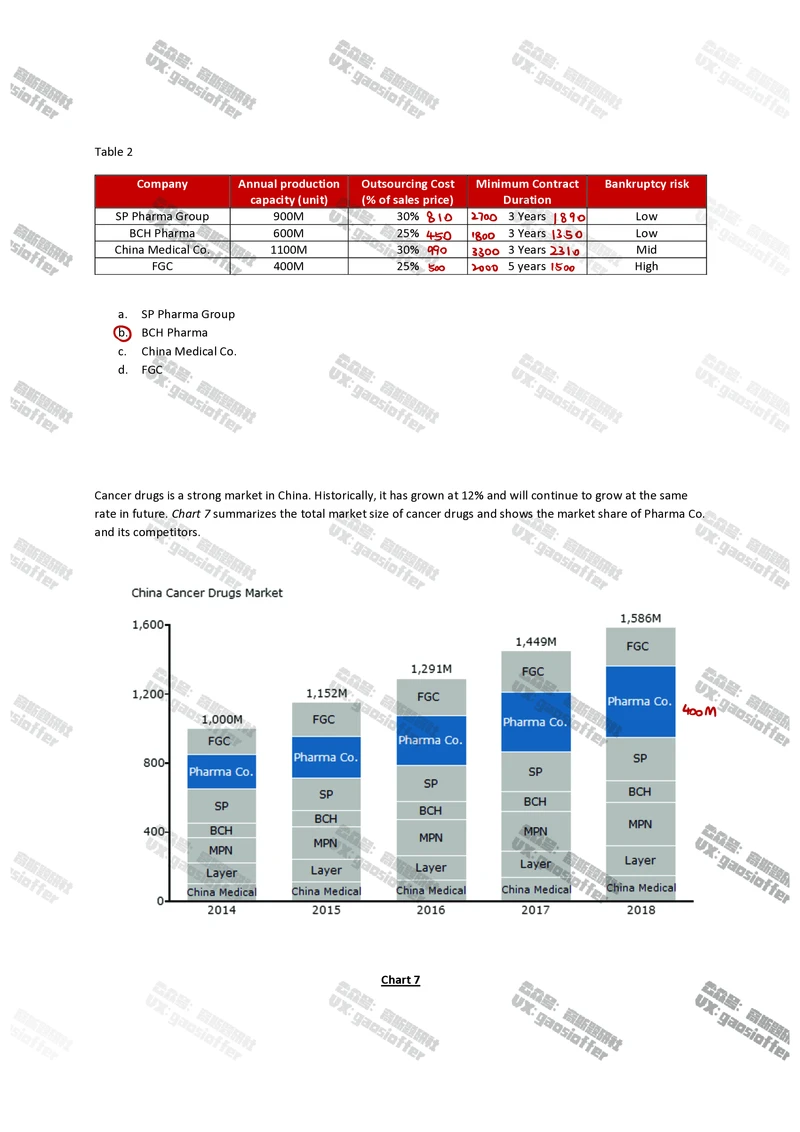

Q22. Assume that Pharma Co. decides to go ahead with second alternative of production, i.e., outsourcing. The

following were the potential companieswith relevant technology under consideration. Which of the following

companies would you outsource production facilities to maximize value for next 3 years?

Assumption: Every consumeris expected to consume100 units of RFC-9000 in a yearTable 2

Company Annual production Outsourcing Cost Minimum Contract Bankruptcy risk

capacity(unit) (% of sales price) Duration

SP Pharma Group 900M 30% 810 2700 3 Years 1890 Low

BCH Pharma 600M 25% 3 Years Low

450 1800 1350

China Medical Co. 1100M 30%990

3300

3 Years2310 Mid

FGC 400M 25%

5 woo

5 years150 High

a. SP Pharma Group

ob. BCH Pharma

c. ChinaMedical Co.

d. FGC

Cancer drugs is a strong market in China. Historically, it has grown at 12% and will continue to grow at the same

rate in future. Chart 7summarizes the total market size of cancer drugs and shows the market share of Pharma Co.

and its competitors.

(cid:4913)

M

Chart 7Q23. If Pharma Co. grows at the rate of 20% every year, what will be the approximate revenues for the company in

this segment in 2018?

a. RMB 415M

b. RMB 240M

oc. RMB 400M

d. Data insufficient

To investigate further, Bain team also conducted interviews with Pharma industry experts. Chart 8 summarizes

some of the inputs that Bain received from these interviews.

Q24. Which of the following cannot be inferred from the following excerpts from interviews?

Chart 8

1. Pharma companies may face issues at developing in house capabilities for producing cancer drugs

2. Once the production facility is outsourced, the outsourcee company has no control over the production

process

3. The decision to outsource production is not focused only on cost related factors

4. Law suits filed by pharma industries relate just to outsourcing agreements

a. Both 1 and 2

ob. Both 2 and 4

c. Only 2

d. Both 3 and 4Q25. Pharma Co. goes ahead with the launch of RFC-9000 in 2016. The drug performs well in the market and

increases company’s total revenues as projected. However, post 2018, the company starts witnessing a slight

decline in sales of cancer drugs, which continues for next several years. Which of the following cannot be a

potential reason for the slow decline in revenues?

1. A competitor has come up with a new drug similar to RFC-9000 priced at a lower level

2. The company has withdrawn RFC-9000 from the market due to a false claim filed by a patient which has also

tarnished the image of the company

3. The industry overall is shrinking

4. Costof the ingredients for cancer drug have increased

(cid:3563)(cid:1609)

a. Only 3

b. Only 4

c. Both 2 and 4

d. All of them