夜雨聆风

夜雨聆风

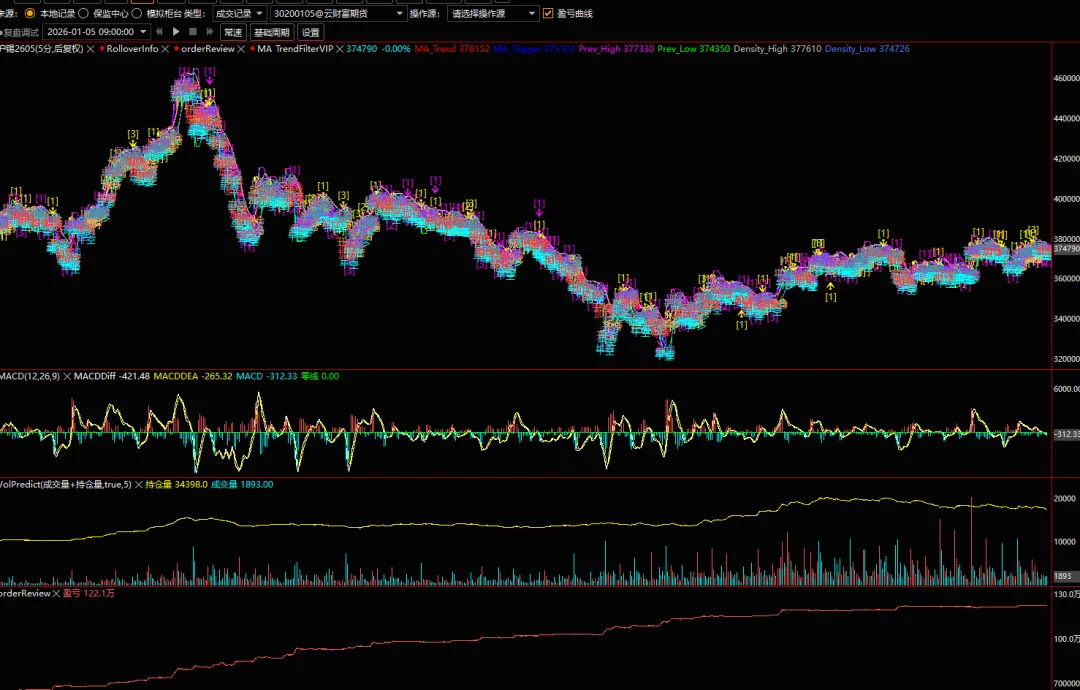

趋势增强策略(附带PY源码)

"""策略名称:趋势过滤策略 (ADX 增强版)策略描述:双均线趋势过滤 + 支撑压力位 + 突破加仓 + ADX 趋势强度开关策略核心逻辑:1. 双均线系统:主趋势均线 (26) + 触发均线 (5)2. ADX 趋势过滤:ADX<25 震荡市禁止开仓,ADX>=25 趋势市允许交易3. 支撑压力位:前高前低 + 交易密集区4. 突破加仓:盈利达到 ATR 倍数后突破压力位可加仓5. 趋势反转:主趋势反转时强制平仓6. 价格修正:针对 next_bar_open 订单,在下一根 K 线确认实际成交价"""import pandas as pdimport numpy as npfrom ssquant.api.strategy_api import StrategyAPIfrom ssquant.backtest.unified_runner import UnifiedStrategyRunner, RunModefrom ssquant.config.trading_config import get_config# ============== 全局状态变量 ==============# 持仓状态g_entry_price = 0 # 入场价格 (实际成交价)g_avg_entry_price = 0 # 平均入场价格(加仓后)g_entry_bar = 0 # 入场 K 线索引g_add_position_count = 0 # 加仓次数# 待确认订单状态 (用于处理 next_bar_open 的价格延迟)g_pending_action = 0 # 0=无,1=开多,-1=开空,2=加多,-2=加空g_pending_old_pos = 0 # 挂单时的旧持仓g_pending_add_lots = 0 # 挂单时的计划加仓手数# 加仓控制g_max_add_times = 2 # 最大加仓次数g_profit_for_add = 1 # 盈利多少倍 ATR 后允许加仓# 到期控制g_expire_date = 20260630 # 到期日期 YYYYMMDDg_enable_expire = False # 是否启用到期控制# 日志控制g_last_log_bar = -100 # 上次日志输出的 K 线索引# ============== 技术指标计算函数 ==============def calculate_atr(high, low, close, period=20):"""计算 ATR (平均真实波幅)"""tr1 = high - lowtr2 = abs(high - close.shift(1))tr3 = abs(low - close.shift(1))tr = pd.concat([tr1, tr2, tr3], axis=1).max(axis=1)return tr.rolling(period).mean()def calculate_adx(high, low, close, period=14):"""计算 ADX (平均趋向指数) - 标准 Wilder's Smoothing 实现- ADX 只衡量趋势强弱,不区分多空方向- ADX < 25: 震荡市 (禁止开仓)- ADX >= 25: 趋势市 (允许开仓)"""# 1. 计算 +DM 和 -DMhigh_diff = high.diff()low_diff = -low.diff()# 原始 DMplus_dm_raw = np.where((high_diff > low_diff) & (high_diff > 0), high_diff, 0)minus_dm_raw = np.where((low_diff > high_diff) & (low_diff > 0), low_diff, 0)# 2. 计算 TRtr1 = high - lowtr2 = abs(high - close.shift(1))tr3 = abs(low - close.shift(1))tr_raw = pd.concat([tr1, tr2, tr3], axis=1).max(axis=1)# 3. 平滑处理 (使用 Rolling Mean 近似 SMA 平滑)tr_smooth = tr_raw.rolling(period).mean()plus_dm_smooth = pd.Series(plus_dm_raw).rolling(period).mean()minus_dm_smooth = pd.Series(minus_dm_raw).rolling(period).mean()# 4. 计算 +DI 和 -DI (防止除以零)plus_di = pd.Series(np.zeros(len(close)))minus_di = pd.Series(np.zeros(len(close)))mask = tr_smooth > 0plus_di[mask] = 100 * plus_dm_smooth[mask] / tr_smooth[mask]minus_di[mask] = 100 * minus_dm_smooth[mask] / tr_smooth[mask]# 5. 计算 DX 和 ADXdi_sum = plus_di + minus_didi_diff = abs(plus_di - minus_di)dx = pd.Series(np.zeros(len(close)))mask_sum = di_sum > 0dx[mask_sum] = 100 * di_diff[mask_sum] / di_sum[mask_sum]adx = dx.rolling(period).mean()return adx, plus_di, minus_didef calculate_donchian(high, low, period=20):"""计算唐奇安通道 (前高前低)"""upper = high.rolling(period).max()lower = low.rolling(period).min()return upper, lowerdef calculate_density_zone(high, low, close, atr, period=30):"""计算交易密集区使用均线作为中心,ATR 作为宽度"""density_mid = close.rolling(period).mean()density_high = density_mid + atr * 2density_low = density_mid - atr * 2return density_high, density_low# ============== 策略初始化函数 ==============def initialize(api: StrategyAPI):"""策略初始化函数,在策略开始前调用一次"""api.log("=" * 60)api.log("MA 趋势过滤策略 (ADX 增强版) 已启动")api.log("=" * 60)# 获取并打印参数length_trend = api.get_param('length_trend', 26)length_trigger = api.get_param('length_trigger', 5)lookback_highlow = api.get_param('lookback_highlow', 20)density_zone_period = api.get_param('density_zone_period', 30)enable_add_position = api.get_param('enable_add_position', 1)max_add_times = api.get_param('max_add_times', 2)add_position_ratio = api.get_param('add_position_ratio', 0.5)profit_for_add = api.get_param('profit_for_add', 1)adx_threshold = api.get_param('adx_threshold', 25)enable_expire = api.get_param('enable_expire', 0)expire_year = api.get_param('expire_year', 2026)expire_month = api.get_param('expire_month', 6)expire_day = api.get_param('expire_day', 30)api.log(f"主趋势均线周期:{length_trend}")api.log(f"触发均线周期:{length_trigger}")api.log(f"前高前低周期:{lookback_highlow}")api.log(f"密集区周期:{density_zone_period}")api.log(f"ADX 趋势阈值:{adx_threshold} (<25 震荡禁止开仓)")api.log(f"突破加仓:{'启用'if enable_add_position == 1else'关闭'}")api.log(f"最大加仓次数:{max_add_times}")api.log(f"加仓手数比例:{add_position_ratio * 100:.0f}%")api.log(f"盈利 ATR 倍数要求:{profit_for_add}")api.log(f"到期时间:{expire_year}-{expire_month:02d}-{expire_day:02d}")api.log(f"到期控制:{'启用'if enable_expire == 1else'关闭'}")api.log("=" * 60)# 设置全局变量global g_max_add_times, g_profit_for_add, g_expire_date, g_enable_expireg_max_add_times = max_add_timesg_profit_for_add = profit_for_addg_expire_date = expire_year * 10000 + expire_month * 100 + expire_dayg_enable_expire = (enable_expire == 1)# ============== 策略主函数 ==============def strategy(api: StrategyAPI):"""策略主函数- 每根 K 线完成时调用"""global g_entry_price, g_avg_entry_price, g_entry_barglobal g_add_position_countglobal g_pending_action, g_pending_old_pos, g_pending_add_lotsglobal g_last_log_bar# ========== 1. 获取参数 ==========length_trend = api.get_param('length_trend', 26)length_trigger = api.get_param('length_trigger', 5)lookback_highlow = api.get_param('lookback_highlow', 20)density_zone_period = api.get_param('density_zone_period', 30)enable_add_position = api.get_param('enable_add_position', 1)add_position_ratio = api.get_param('add_position_ratio', 0.5)adx_threshold = api.get_param('adx_threshold', 25)enable_expire = api.get_param('enable_expire', 0)# ========== 2. 数据检查 ==========min_bars = max(length_trend, density_zone_period, 14) + 10 # ADX 需要 14+periodif api.get_idx() < min_bars:return# ========== 3. 获取 K 线数据 ==========close = api.get_close()high = api.get_high()low = api.get_low()open_price = api.get_open()if close is None or len(close) < min_bars:returncurrent_price = close.iloc[-1]current_open = open_price.iloc[-1] # 当前 K 线开盘价 (即上一根 K 线 next_bar_open 的实际成交价)current_dt = api.get_datetime()# ========== 3.5 处理上一根 K 线的挂单成交 (核心修复) ==========# 如果是 next_bar_open 下单,实际成交价是当前 K 线的开盘价# 在此处更新全局状态,确保后续盈亏计算基于真实成本if g_pending_action != 0:pos = api.get_pos()if g_pending_action == 1: # 开多成交g_entry_price = current_openg_avg_entry_price = current_openg_entry_bar = api.get_idx()api.log(f"✅ 多头开仓成交 | 价格:{current_open:.2f}")elif g_pending_action == -1: # 开空成交g_entry_price = current_openg_avg_entry_price = current_openg_entry_bar = api.get_idx()api.log(f"✅ 空头开仓成交 | 价格:{current_open:.2f}")elif g_pending_action == 2: # 加多成交if pos > 0 and g_pending_old_pos > 0:# 准确计算新均价:(旧总成本 + 新成本) / 新总手数g_avg_entry_price = (g_avg_entry_price * g_pending_old_pos + current_open * g_pending_add_lots) / posapi.log(f"✅ 多头加仓成交 | 价格:{current_open:.2f} | 新均价:{g_avg_entry_price:.2f}")elif g_pending_action == -2: # 加空成交if pos < 0 and g_pending_old_pos < 0:# 注意 pos 和 old_pos 都是负数,计算时取绝对值g_avg_entry_price = (g_avg_entry_price * abs(g_pending_old_pos) + current_open * g_pending_add_lots) / abs(pos)api.log(f"✅ 空头加仓成交 | 价格:{current_open:.2f} | 新均价:{g_avg_entry_price:.2f}")# 清空 pending 状态g_pending_action = 0g_pending_old_pos = 0g_pending_add_lots = 0# ========== 4. 检查到期时间 ==========if enable_expire == 1 and current_dt is not None:current_date = current_dt.year * 10000 + current_dt.month * 100 + current_dt.dayif current_date >= g_expire_date:pos = api.get_pos()if pos > 0:api.sell(order_type='next_bar_open', reason='策略到期强制平多')api.log(f"⚠️ 策略已到期,强制平多仓")elif pos < 0:api.buycover(order_type='next_bar_open', reason='策略到期强制平空')api.log(f"⚠️ 策略已到期,强制平空仓")g_entry_price = 0g_avg_entry_price = 0g_add_position_count = 0return# ========== 5. 计算技术指标 ==========# 5.1 均线ma_trend = close.rolling(length_trend).mean()ma_trigger = close.rolling(length_trigger).mean()# 5.2 ATRatr_value = calculate_atr(high, low, close, 20)# 5.3 ADX (趋势强度指标)adx, plus_di, minus_di = calculate_adx(high, low, close, 14)# 5.4 支撑压力位prev_high, prev_low = calculate_donchian(high, low, lookback_highlow)density_high, density_low = calculate_density_zone(high, low, close, atr_value, density_zone_period)# 检查 NaN 值if pd.isna(ma_trend.iloc[-1]) or pd.isna(ma_trigger.iloc[-1]) or pd.isna(atr_value.iloc[-1]) or pd.isna(adx.iloc[-1]):return# ========== 6. 判断趋势状态 ==========# 主趋势方向is_long_trend = current_price > ma_trend.iloc[-1]is_short_trend = current_price < ma_trend.iloc[-1]# ADX 趋势强度过滤adx_current = adx.iloc[-1]adx_prev = adx.iloc[-2] if len(adx) >= 2 else adx_currentadx_turning_up = adx_current > adx_prevadx_turning_down = adx_current < adx_prev# 趋势市判断 (ADX >= 阈值)is_trend_market = adx_current >= adx_threshold# ========== 7. 交叉信号 ==========cross_up_trigger = (close.iloc[-2] <= ma_trigger.iloc[-2] andclose.iloc[-1] > ma_trigger.iloc[-1])cross_down_trigger = (close.iloc[-2] >= ma_trigger.iloc[-2] andclose.iloc[-1] < ma_trigger.iloc[-1])# ========== 8. 突破信号 ==========break_high = current_price > prev_high.iloc[-2]break_low = current_price < prev_low.iloc[-2]break_density_high = current_price > density_high.iloc[-2]break_density_low = current_price < density_low.iloc[-2]# ========== 9. 持仓和盈亏计算 ==========pos = api.get_pos()# 计算当前盈利 ATR 倍数profit_atr = 0if pos > 0 and g_avg_entry_price > 0 and atr_value.iloc[-1] > 0:profit_atr = (current_price - g_avg_entry_price) / atr_value.iloc[-1]elif pos < 0 and g_avg_entry_price > 0 and atr_value.iloc[-1] > 0:profit_atr = (g_avg_entry_price - current_price) / atr_value.iloc[-1]# ========== 10. 资金管理 ==========base_lots = 1add_lots = max(1, int(base_lots * add_position_ratio))# ========== 11. 交易逻辑 ==========# --- 开仓逻辑 (受 ADX 严格过滤) ---# 只有当是趋势市 (ADX>=25) 时才允许开新仓if is_trend_market:# 多头开仓if is_long_trend and cross_up_trigger and pos <= 0:if pos < 0:api.buycover(order_type='next_bar_open', reason='平空开多')api.buy(volume=base_lots, order_type='next_bar_open', reason='多头趋势上穿触发均线')# 标记 pending 状态,等待下一根 K 线确认价格g_pending_action = 1g_pending_old_pos = posg_pending_add_lots = base_lotsapi.log(f"📈 发出多头开仓指令 | 信号价:{current_price:.2f} | ADX:{adx_current:.2f}")# 空头开仓elif is_short_trend and cross_down_trigger and pos >= 0:if pos > 0:api.sell(order_type='next_bar_open', reason='平多开空')api.sellshort(volume=base_lots, order_type='next_bar_open', reason='空头趋势下穿触发均线')# 标记 pending 状态g_pending_action = -1g_pending_old_pos = posg_pending_add_lots = base_lotsapi.log(f"📉 发出空头开仓指令 | 信号价:{current_price:.2f} | ADX:{adx_current:.2f}")# --- 加仓逻辑 (受 ADX 过滤) ---elif enable_add_position == 1 and g_add_position_count < g_max_add_times:# 多头加仓if pos > 0:if break_high and profit_atr >= g_profit_for_add:api.buy(volume=add_lots, order_type='next_bar_open', reason='突破前高加仓')g_pending_action = 2g_pending_old_pos = posg_pending_add_lots = add_lotsapi.log(f"➕ 发出多头加仓指令 | 信号价:{current_price:.2f}")elif break_density_high and profit_atr >= g_profit_for_add:api.buy(volume=add_lots, order_type='next_bar_open', reason='突破密集区加仓')g_pending_action = 2g_pending_old_pos = posg_pending_add_lots = add_lotsapi.log(f"➕ 发出多头加仓指令 (密集区) | 信号价:{current_price:.2f}")# 空头加仓elif pos < 0:if break_low and profit_atr >= g_profit_for_add:api.sellshort(volume=add_lots, order_type='next_bar_open', reason='突破前低加仓')g_pending_action = -2g_pending_old_pos = posg_pending_add_lots = add_lotsapi.log(f"➕ 发出空头加仓指令 | 信号价:{current_price:.2f}")elif break_density_low and profit_atr >= g_profit_for_add:api.sellshort(volume=add_lots, order_type='next_bar_open', reason='突破密集区加仓')g_pending_action = -2g_pending_old_pos = posg_pending_add_lots = add_lotsapi.log(f"➕ 发出空头加仓指令 (密集区) | 信号价:{current_price:.2f}")# --- 平仓逻辑 (不受 ADX 限制,只要持仓且触发信号即平仓) ---# 修复:将平仓逻辑移出 ADX 过滤块,避免震荡市无法止损# 多头平仓:下穿触发均线if pos > 0 and cross_down_trigger and (api.get_idx() - g_entry_bar) >= 1:api.sell(order_type='next_bar_open', reason='下穿触发均线平仓')pnl = current_price - g_avg_entry_priceclose_type = "止损" if pnl < 0 else "止盈"api.log(f"📉 发出多头平仓指令 ({close_type}) | 均价:{g_avg_entry_price:.2f} | 信号价:{current_price:.2f}")g_add_position_count = 0# 注意:价格和状态将在成交后或反转时重置,这里先不重置以避免逻辑冲突# 空头平仓:上穿触发均线elif pos < 0 and cross_up_trigger and (api.get_idx() - g_entry_bar) >= 1:api.buycover(order_type='next_bar_open', reason='上穿触发均线平仓')pnl = g_avg_entry_price - current_priceclose_type = "止损" if pnl < 0 else "止盈"api.log(f"📈 发出空头平仓指令 ({close_type}) | 均价:{g_avg_entry_price:.2f} | 信号价:{current_price:.2f}")g_add_position_count = 0# --- 趋势反转强制平仓 (不受 ADX 限制) ---# 多头持仓但主趋势转空if pos > 0 and not is_long_trend:api.sell(order_type='next_bar_open', reason='主趋势转空强制平仓')pnl = current_price - g_avg_entry_priceclose_type = "止损" if pnl < 0 else "止盈"api.log(f"⚠️ 发出趋势反转强制平多指令 ({close_type}) | 均价:{g_avg_entry_price:.2f}")g_entry_price = 0g_avg_entry_price = 0g_add_position_count = 0# 空头持仓但主趋势转多elif pos < 0 and not is_short_trend:api.buycover(order_type='next_bar_open', reason='主趋势转多强制平仓')pnl = g_avg_entry_price - current_priceclose_type = "止损" if pnl < 0 else "止盈"api.log(f"⚠️ 发出趋势反转强制平空指令 ({close_type}) | 均价:{g_avg_entry_price:.2f}")g_entry_price = 0g_avg_entry_price = 0g_add_position_count = 0# 如果当前无持仓,清理残留状态if pos == 0 and g_avg_entry_price != 0 and g_pending_action == 0:g_avg_entry_price = 0g_entry_price = 0# ========== 12. 定期状态输出 ==========current_idx = api.get_idx()if current_idx % 100 == 0 and current_idx != g_last_log_bar:adx_status = "趋势市" if is_trend_market else "震荡市 (禁止开仓)"adx_direction = "↗增强" if adx_turning_up else ("↘减弱" if adx_turning_down else "→持平")api.log(f"[状态] K 线:{current_idx} | 趋势:{adx_status} | ADX:{adx_current:.2f}{adx_direction} | 持仓:{pos}")g_last_log_bar = current_idx# ========== 13. 图表注释 ==========if current_idx % 10 == 0:adx_status = "趋势市" if is_trend_market else "震荡市"trend_dir = "多头" if is_long_trend else ("空头" if is_short_trend else "震荡")api.log(f"[注释] 趋势:{trend_dir} | 市场:{adx_status} | ADX:{adx_current:.2f} | 持仓:{pos}手 | 加仓:{g_add_position_count}/{g_max_add_times}")# ============== 主函数 ==============if __name__ == "__main__":# ========== 运行模式 ==========RUN_MODE = RunMode.BACKTEST# ========== 策略参数 ==========strategy_params = {# 均线参数'length_trend': 26, # 主趋势均线周期'length_trigger': 5, # 触发交易均线周期# 支撑压力参数'lookback_highlow': 20, # 前高前低回溯周期'density_zone_period': 30, # 交易密集区统计周期# 加仓参数'enable_add_position': 1, # 是否启用突破加仓 (1=启用,0=关闭)'max_add_times': 2, # 最大加仓次数'add_position_ratio': 0.5, # 加仓手数比例 (0.5=半仓加仓)'profit_for_add': 1, # 盈利多少倍 ATR 后允许加仓# ADX 趋势过滤参数'adx_threshold': 25, # ADX 趋势阈值 (<25 震荡,>=25 趋势)# 到期时间设置'enable_expire': 0, # 是否启用到期时间 (1=启用,0=不启用)'expire_year': 2026, # 到期年份'expire_month': 6, # 到期月份'expire_day': 30, # 到期日期}# ========== 配置 ==========if RUN_MODE == RunMode.BACKTEST:config = get_config(RUN_MODE,# -------- 合约与周期 --------symbol='rb888', # 主力连续合约kline_period='5m', # K 线周期adjust_type='1', # 后复权# -------- 数据范围 --------start_date='2025-01-01',end_date='2025-12-31',# -------- 回测参数 --------initial_capital=100000, # 初始资金slippage_ticks=1, # 滑点# -------- 数据窗口 --------lookback_bars=500,debug=False,)elif RUN_MODE == RunMode.SIMNOW:config = get_config(RUN_MODE,account='simnow_default',server_name='电信 1',symbol='rb888',kline_period='5m',order_offset_ticks=5,algo_trading=False,preload_history=True,history_lookback_bars=100,adjust_type='1',lookback_bars=500,enable_tick_callback=False,)elif RUN_MODE == RunMode.REAL_TRADING:config = get_config(RUN_MODE,account='real_default',symbol='rb888',kline_period='5m',order_offset_ticks=5,algo_trading=True,preload_history=True,history_lookback_bars=100,adjust_type='1',lookback_bars=500,)# ========== 运行 ==========print(f"\n运行模式:{RUN_MODE.value}")print(f"合约代码:{config.get('symbol', 'N/A')}")runner = UnifiedStrategyRunner(mode=RUN_MODE)runner.set_config(config)try:results = runner.run(strategy=strategy,initialize=initialize,strategy_params=strategy_params)except KeyboardInterrupt:print("\n用户中断")runner.stop()except Exception as e:print(f"\n运行出错:{e}")import tracebacktraceback.print_exc()runner.stop()